Ames Housing Data Processing, analysis and predictive modeling

Predictive modeling

In a previous notebook we processed and cleaned the Ames dataset, and in another we explored the data.

In this notebook, we’ll model and predict SalePrice. First we’ll do a little feature selection and engineering to create a few different versions of the data for modeling. Then we’ll compare the prediction performance of some appropriate models on these versions, select a subset of these versions and models for fine-tuning, ensemble them to maximize predictive generalizablity, and test them by submitting to Kaggle.

Contents

- Setup

- Load and prepare data

- Feature selection and engineering

- Model selection and tuning

- Predict and Evaluate

Setup

%matplotlib inline

import warnings

import os

import sys

import time

import hyperopt.hp as hp

from sklearn.linear_model import LinearRegression, Lasso, Ridge, BayesianRidge

from sklearn.cross_decomposition import PLSRegression

from sklearn.svm import SVR

from sklearn.neighbors import KNeighborsRegressor

from sklearn.neural_network import MLPRegressor

from sklearn.tree import DecisionTreeRegressor, ExtraTreeRegressor

from hyperopt.pyll import scope as ho_scope

# add parent directory for importing custom classes

pardir = os.path.abspath(os.path.join(os.getcwd(), os.pardir))

sys.path.append(pardir)

# custom classes and helpers

from codes.process import DataDescription, HPDataFramePlus, DataPlus

from codes.explore import load_datasets, plot_cont_dists

from codes.model import *

warnings.filterwarnings('ignore')

plt.style.use('seaborn-white')

sns.set_style('white')

Load and prepare data

hp_data = load_datasets(data_dir='../data', file_names=['clean.csv'])

clean = hp_data.dfs['clean']

The dataset clean was created in a previous notebook. It is the original dataset with some problematic variables and observations dropped and missing values imputed. We’ll use it to create our modeling data

Feature selection and engineering

We’ll use the results of our exploratory analysis to suggest variables that can be altered, combined, or eliminated in the hopes of improving predictive models. We’ll create a few new datasets in the process. In the end we’ll have four versions of the data for modeling

clean: original dataset with problematic features and observations dropped and missing values imputed.drop:cleandataset with some old features droppedclean_edit:cleandataset with some feature values combined and some new features addeddrop_edit:dropdataset with the same feature values combined and same new features added.

Drop some features

Here are variables we’ll drop (and the reasons for dropping):

Heating,RoofMatl,Condition2,Street(extremely unbalanced distributions and very low dependence withSalePrice())Exterior2nd(redundant withExterior1st.HouseStyle(redundant withMSSubclass).Utilities(extremely unbalanced distribution and very low dependence with response)PoolQC(extremely unbalanced distribution and redundant withPoolArea)1stFlrSFandTotalBsmtSF(high dependence withGrLivArea).GarageYrBlt(high dependence withYearBuilt)PoolArea,MiscVal,3SsnPorch,ScreenPorch,BsmtFinSF2(extremely peaked distributions and very low dependence withSalePrice)LowQualFinSF(extremely peaked distribution and redundant with ordinal quality measures such asOverallQual)

drop_cols = ['Heating', 'RoofMatl', 'Condition2', 'Street', 'Exterior2nd', 'HouseStyle',

'Utilities', 'PoolQC', '1stFlrSF', 'TotalBsmtSF', 'GarageYrBlt', 'PoolArea', 'MiscVal',

'3SsnPorch', 'ScreenPorch', 'BsmtFinSF2', 'LowQualFinSF']

drop = HPDataFramePlus(data=clean.data)

drop.data = drop.data.drop(columns=drop_cols)

drop.data.columns

Index(['MSSubClass', 'MSZoning', 'LotFrontage', 'LotArea', 'LotShape',

'LandContour', 'LotConfig', 'LandSlope', 'Neighborhood', 'Condition1',

'BldgType', 'OverallQual', 'OverallCond', 'YearBuilt', 'YearRemodAdd',

'RoofStyle', 'Exterior1st', 'MasVnrType', 'MasVnrArea', 'ExterQual',

'ExterCond', 'Foundation', 'BsmtQual', 'BsmtCond', 'BsmtExposure',

'BsmtFinType1', 'BsmtFinSF1', 'BsmtFinType2', 'BsmtUnfSF', 'HeatingQC',

'CentralAir', 'Electrical', '2ndFlrSF', 'GrLivArea', 'BsmtFullBath',

'BsmtHalfBath', 'FullBath', 'HalfBath', 'BedroomAbvGr', 'KitchenAbvGr',

'KitchenQual', 'TotRmsAbvGrd', 'Functional', 'Fireplaces',

'FireplaceQu', 'GarageType', 'GarageFinish', 'GarageCars', 'GarageArea',

'GarageQual', 'GarageCond', 'PavedDrive', 'WoodDeckSF', 'OpenPorchSF',

'EnclosedPorch', 'Fence', 'MoSold', 'YrSold', 'SaleType',

'SaleCondition', 'SalePrice'],

dtype='object')

Combine values and create new variables

Some discrete variables had very small counts for some values (this could be seen as horizontal lines corresponding to those values in the violin plots for categorical and ordinal variables.

First we’ll look at categorical variables

cats_data = clean.data.select_dtypes('category')

cats_data.columns

Index(['MSSubClass', 'MSZoning', 'Street', 'LandContour', 'LotConfig',

'Neighborhood', 'Condition1', 'Condition2', 'BldgType', 'HouseStyle',

'RoofStyle', 'RoofMatl', 'Exterior1st', 'Exterior2nd', 'MasVnrType',

'Foundation', 'Heating', 'CentralAir', 'Electrical', 'GarageType',

'SaleType', 'SaleCondition'],

dtype='object')

# print variables with less than 5 observations for any value

small_val_count_cat_cols = print_small_val_counts(data=cats_data, val_count_threshold=6)

20 1078

60 573

50 287

120 182

30 139

70 128

160 128

80 118

90 109

190 61

85 48

75 23

45 18

180 17

40 6

150 1

Name: MSSubClass, dtype: int64

Norm 2887

Feedr 13

Artery 5

PosA 4

PosN 3

RRNn 2

RRAn 1

RRAe 1

Name: Condition2, dtype: int64

Gable 2310

Hip 549

Gambrel 22

Flat 19

Mansard 11

Shed 5

Name: RoofStyle, dtype: int64

CompShg 2875

Tar&Grv 22

WdShake 9

WdShngl 7

Roll 1

Metal 1

Membran 1

Name: RoofMatl, dtype: int64

VinylSd 1026

MetalSd 450

HdBoard 442

Wd Sdng 411

Plywood 220

CemntBd 125

BrkFace 87

WdShing 56

AsbShng 44

Stucco 42

BrkComm 6

Stone 2

CBlock 2

AsphShn 2

ImStucc 1

Name: Exterior1st, dtype: int64

VinylSd 1015

MetalSd 447

HdBoard 406

Wd Sdng 391

Plywood 269

CmentBd 125

Wd Shng 81

BrkFace 47

Stucco 46

AsbShng 38

Brk Cmn 22

ImStucc 15

Stone 6

AsphShn 4

CBlock 3

Other 1

Name: Exterior2nd, dtype: int64

None 1761

BrkFace 945

Stone 205

BrkCmn 5

Name: MasVnrType, dtype: int64

PConc 1306

CBlock 1234

BrkTil 311

Slab 49

Stone 11

Wood 5

Name: Foundation, dtype: int64

GasA 2871

GasW 27

Grav 9

Wall 6

OthW 2

Floor 1

Name: Heating, dtype: int64

SBrkr 2669

FuseA 188

FuseF 50

FuseP 8

Mix 1

Name: Electrical, dtype: int64

WD 2525

New 237

COD 87

ConLD 26

CWD 12

ConLI 9

ConLw 8

Oth 7

Con 5

Name: SaleType, dtype: int64

desc = DataDescription('../data/data_description.txt')

clean.desc = desc

clean.print_desc(small_val_count_cat_cols)

MSSubClass: Identifies the type of dwelling involved in the sale.

20 - 1-STORY 1946 & NEWER ALL STYLES

30 - 1-STORY 1945 & OLDER

40 - 1-STORY W/FINISHED ATTIC ALL AGES

45 - 1-1/2 STORY - UNFINISHED ALL AGES

50 - 1-1/2 STORY FINISHED ALL AGES

60 - 2-STORY 1946 & NEWER

70 - 2-STORY 1945 & OLDER

75 - 2-1/2 STORY ALL AGES

80 - SPLIT OR MULTI-LEVEL

85 - SPLIT FOYER

90 - DUPLEX - ALL STYLES AND AGES

120 - 1-STORY PUD (Planned Unit Development) - 1946 & NEWER

150 - 1-1/2 STORY PUD - ALL AGES

160 - 2-STORY PUD - 1946 & NEWER

180 - PUD - MULTILEVEL - INCL SPLIT LEV/FOYER

190 - 2 FAMILY CONVERSION - ALL STYLES AND AGES

Condition2: Proximity to various conditions (if more than one is present)

Artery - Adjacent to arterial street

Feedr - Adjacent to feeder street

Norm - Normal

RRNn - Within 200' of North-South Railroad

RRAn - Adjacent to North-South Railroad

PosN - Near positive off-site feature--park, greenbelt, etc.

PosA - Adjacent to postive off-site feature

RRNe - Within 200' of East-West Railroad

RRAe - Adjacent to East-West Railroad

RoofStyle: Type of roof

Flat - Flat

Gable - Gable

Gambrel - Gabrel (Barn)

Hip - Hip

Mansard - Mansard

Shed - Shed

RoofMatl: Roof material

ClyTile - Clay or Tile

CompShg - Standard (Composite) Shingle

Membran - Membrane

Metal - Metal

Roll - Roll

Tar&Grv - Gravel & Tar

WdShake - Wood Shakes

WdShngl - Wood Shingles

Exterior1st: Exterior covering on house

AsbShng - Asbestos Shingles

AsphShn - Asphalt Shingles

BrkComm - Brick Common

BrkFace - Brick Face

CBlock - Cinder Block

CemntBd - Cement Board

HdBoard - Hard Board

ImStucc - Imitation Stucco

MetalSd - Metal Siding

Other - Other

Plywood - Plywood

PreCast - PreCast

Stone - Stone

Stucco - Stucco

VinylSd - Vinyl Siding

Sdng - Wood Siding

WdShing - Wood Shingles

Exterior2nd: Exterior covering on house (if more than one material)

AsbShng - Asbestos Shingles

AsphShn - Asphalt Shingles

BrkComm - Brick Common

BrkFace - Brick Face

CBlock - Cinder Block

CemntBd - Cement Board

HdBoard - Hard Board

ImStucc - Imitation Stucco

MetalSd - Metal Siding

Other - Other

Plywood - Plywood

PreCast - PreCast

Stone - Stone

Stucco - Stucco

VinylSd - Vinyl Siding

Sdng - Wood Siding

WdShing - Wood Shingles

MasVnrType: Masonry veneer type

BrkCmn - Brick Common

BrkFace - Brick Face

CBlock - Cinder Block

None - None

Stone - Stone

Foundation: Type of foundation

BrkTil - Brick & Tile

CBlock - Cinder Block

PConc - Poured Contrete

Slab - Slab

Stone - Stone

Wood - Wood

Heating: Type of heating

Floor - Floor Furnace

GasA - Gas forced warm air furnace

GasW - Gas hot water or steam heat

Grav - Gravity furnace

OthW - Hot water or steam heat other than gas

Wall - Wall furnace

Electrical: Electrical system

SBrkr - Standard Circuit Breakers & Romex

FuseA - Fuse Box over 60 AMP and all Romex wiring (Average)

FuseF - 60 AMP Fuse Box and mostly Romex wiring (Fair)

FuseP - 60 AMP Fuse Box and mostly knob & tube wiring (poor)

Mix - Mixed

SaleType: Type of sale

WD - Warranty Deed - Conventional

CWD - Warranty Deed - Cash

VWD - Warranty Deed - VA Loan

New - Home just constructed and sold

COD - Court Officer Deed/Estate

Con - Contract 15% Down payment regular terms

ConLw - Contract Low Down payment and low interest

ConLI - Contract Low Interest

ConLD - Contract Low Down

Oth - Other

We’ll perform the following combinations of categorical variable values:

-

MSSubClass: Change the single observation with value 150 to 50, the next most sensible value Condition2: MergePosA,PosN,RRNn,RRAn, andRRAeinto a new valueOtherRoofMatl: MergeWdShake,WdShingleinto a new valueWoodandRoll,Metal,Membraninto a new valueOtherExterior1st, : MergeBrkCommintoBrkFace,AsphShnintoAsbShng,ImStuccintoStuccoandStoneandCBlockinto a new valueOtherExterior2nd: MergeAsphShnintoAsbShngandStoneandCBlockintoOther-

Heating: MergeWall,OthW, andFloorinto a new variableOther MasVnrType: MergeBrkComminBrkFaceElectrical: MergeFuseA,FuseF,FuseP, andMixinto a new valueNonStd

# new dataframes

clean_edit = HPDataFramePlus(data=clean.data)

drop_edit = HPDataFramePlus(data=drop.data)

# combine categorical variable values

clean_edit.data = combine_cat_vars(data=clean.data)

drop_edit.data = combine_cat_vars(data=drop.data)

Now we’ll look at ordinal variables

# print small value counts of ordinal variables

edit_ords_data = clean.data.select_dtypes('int64')

small_val_count_ord_cols = print_small_val_counts(edit_ords_data, val_count_threshold=6)

3 2915

1 1

Name: Utilities, dtype: int64

5 825

6 731

7 600

8 342

4 225

9 107

3 40

10 29

2 13

1 4

Name: OverallQual, dtype: int64

3 2535

4 299

2 67

5 12

1 3

Name: ExterCond, dtype: int64

3 2603

4 122

2 104

0 82

1 5

Name: BsmtCond, dtype: int64

5 1490

3 857

4 474

2 92

1 3

Name: HeatingQC, dtype: int64

0 1707

1 1170

2 37

3 2

Name: BsmtFullBath, dtype: int64

0 2741

1 171

2 4

Name: BsmtHalfBath, dtype: int64

2 1529

1 1308

3 63

0 12

4 4

Name: FullBath, dtype: int64

3 1594

2 741

4 400

1 103

5 48

6 21

0 8

8 1

Name: BedroomAbvGr, dtype: int64

1 2782

2 129

0 3

3 2

Name: KitchenAbvGr, dtype: int64

2 1492

3 1150

4 203

1 70

0 1

Name: KitchenQual, dtype: int64

6 843

7 649

5 583

8 347

4 196

9 143

10 80

11 31

3 25

12 15

15 1

13 1

14 1

2 1

Name: TotRmsAbvGrd, dtype: int64

6 2717

3 70

5 64

2 35

4 19

1 9

0 2

Name: Functional, dtype: int64

0 1420

1 1267

2 218

3 10

4 1

Name: Fireplaces, dtype: int64

2 1593

1 776

3 373

0 157

4 16

5 1

Name: GarageCars, dtype: int64

3 2601

0 159

2 124

4 24

1 5

5 3

Name: GarageQual, dtype: int64

3 2651

0 159

2 74

4 15

1 14

5 3

Name: GarageCond, dtype: int64

0 2907

4 4

3 3

1 2

Name: PoolQC, dtype: int64

clean.print_desc(small_val_count_ord_cols)

Utilities: Type of utilities available

AllPub - All public Utilities (E,G,W,& S)

NoSewr - Electricity, Gas, and Water (Septic Tank)

NoSeWa - Electricity and Gas Only

ELO - Electricity only

OverallQual: Rates the overall material and finish of the house

10 - Very Excellent

9 - Excellent

8 - Very Good

7 - Good

6 - Above Average

5 - Average

4 - Below Average

3 - Fair

2 - Poor

1 - Very Poor

ExterCond: Evaluates the present condition of the material on the exterior

Ex - Excellent

Gd - Good

TA - Average/Typical

Fa - Fair

Po - Poor

BsmtCond: Evaluates the general condition of the basement

Ex - Excellent

Gd - Good

TA - Typical - slight dampness allowed

Fa - Fair - dampness or some cracking or settling

Po - Poor - Severe cracking, settling, or wetness

NA - No Basement

HeatingQC: Heating quality and condition

Ex - Excellent

Gd - Good

TA - Average/Typical

Fa - Fair

Po - Poor

BsmtFullBath: Basement full bathrooms

BsmtHalfBath: Basement half bathrooms

FullBath: Full bathrooms above grade

BedroomAbvGr: Bedrooms above grade (does NOT include basement bedrooms)

KitchenAbvGr: Kitchens above grade

KitchenQual: Kitchen quality

Ex - Excellent

Gd - Good

TA - Typical/Average

Fa - Fair

Po - Poor

TotRmsAbvGrd: Total rooms above grade (does not include bathrooms)

Functional: Home functionality (Assume typical unless deductions are warranted)

Typ - Typical Functionality

Min1 - Minor Deductions 1

Min2 - Minor Deductions 2

Mod - Moderate Deductions

Maj1 - Major Deductions 1

Maj2 - Major Deductions 2

Sev - Severely Damaged

Sal - Salvage only

Fireplaces: Number of fireplaces

GarageCars: Size of garage in car capacity

GarageQual: Garage quality

Ex - Excellent

Gd - Good

TA - Typical/Average

Fa - Fair

Po - Poor

NA - No Garage

GarageCond: Garage condition

Ex - Excellent

Gd - Good

TA - Typical/Average

Fa - Fair

Po - Poor

NA - No Garage

PoolQC: Pool quality

Ex - Excellent

Gd - Good

TA - Average/Typical

Fa - Fair

NA - No Pool

Even though many ordinal variables have values with low counts, we’re less inclined to combine values because we lose ordering information. However we will drop Utilities from all data, since a binary variable with one observation for one value is essentially useless.

# drop extremely unbalanced binary variable

clean.data = clean.data.drop(columns=['Utilities'])

clean_edit.data = clean_edit.data.drop(columns=['Utilities'])

We’ll also create some new variables:

Bath=HalfBath+ 2 *FullBathand dropHalfBathandFullBathBsmtBath=BsmtHalfBath+ 2 *BsmtFullBathand dropBsmtHalfBathandBsmtFullBathAvgQual, the average ofOverallQual,ExterQual,BsmtQual,HeatingQC,KitchenQual,FireplaceQuandGarageQual.AvgCond, the average ofOverallCond,ExterCond,BsmtCond, andGarageCond- Indicator variables

HasBsmt,HasFireplace,HasPool,HasGarage,HasFence

Note the factor of 2 in the new bath variables is so full baths are twice the weight of half baths. Also note the new average quality and condition variables will be quantitative (float64 dtype)

# create new ordinal variables

clean_edit.data = create_ord_vars(clean_edit.data, clean.data)

drop_edit.data = create_ord_vars(drop_edit.data, clean.data)

Finally, we’ll look at quantitative variables.

quants_data = clean.data.select_dtypes('float64')

quants_data.columns

Index(['LotFrontage', 'LotArea', 'YearBuilt', 'YearRemodAdd', 'MasVnrArea',

'BsmtFinSF1', 'BsmtFinSF2', 'BsmtUnfSF', 'TotalBsmtSF', '1stFlrSF',

'2ndFlrSF', 'LowQualFinSF', 'GrLivArea', 'GarageYrBlt', 'GarageArea',

'WoodDeckSF', 'OpenPorchSF', 'EnclosedPorch', '3SsnPorch',

'ScreenPorch', 'PoolArea', 'MiscVal', 'SalePrice'],

dtype='object')

We noted above that many of these variables have high concentrations at zero. We’ll

- Create indicator variables

Has2ndFlr,HasWoodDeck,HasPorch - Create an overall area variable

OverallArea=LotArea+GrLivArea+GarageArea - Create a lot variable

LotRatio=LotArea/LotFrontage

# create new quantiative variables

clean_edit.data = create_quant_vars(clean_edit.data, clean.data)

drop_edit.data = create_quant_vars(drop_edit.data, clean.data)

Transform skewed quantitative variables

We noted that many of the quantitative variables (including the response variable SalePrice) had approximately logarithmic distributions, so we’ll apply a log transformation to these. Note that we expect this to improve the performance of some predictive modeling methods (e.g. linear regression) but to have little effect on other methods (e.g. tree-based methods).

quants_data = clean_edit.data.select_dtypes('float64')

quants_data.columns

Index(['LotFrontage', 'LotArea', 'YearBuilt', 'YearRemodAdd', 'MasVnrArea',

'BsmtFinSF1', 'BsmtFinSF2', 'BsmtUnfSF', 'TotalBsmtSF', '1stFlrSF',

'2ndFlrSF', 'LowQualFinSF', 'GrLivArea', 'GarageYrBlt', 'GarageArea',

'WoodDeckSF', 'OpenPorchSF', 'EnclosedPorch', '3SsnPorch',

'ScreenPorch', 'PoolArea', 'MiscVal', 'SalePrice', 'AvgQual', 'AvgCond',

'OverallArea', 'LotRatio'],

dtype='object')

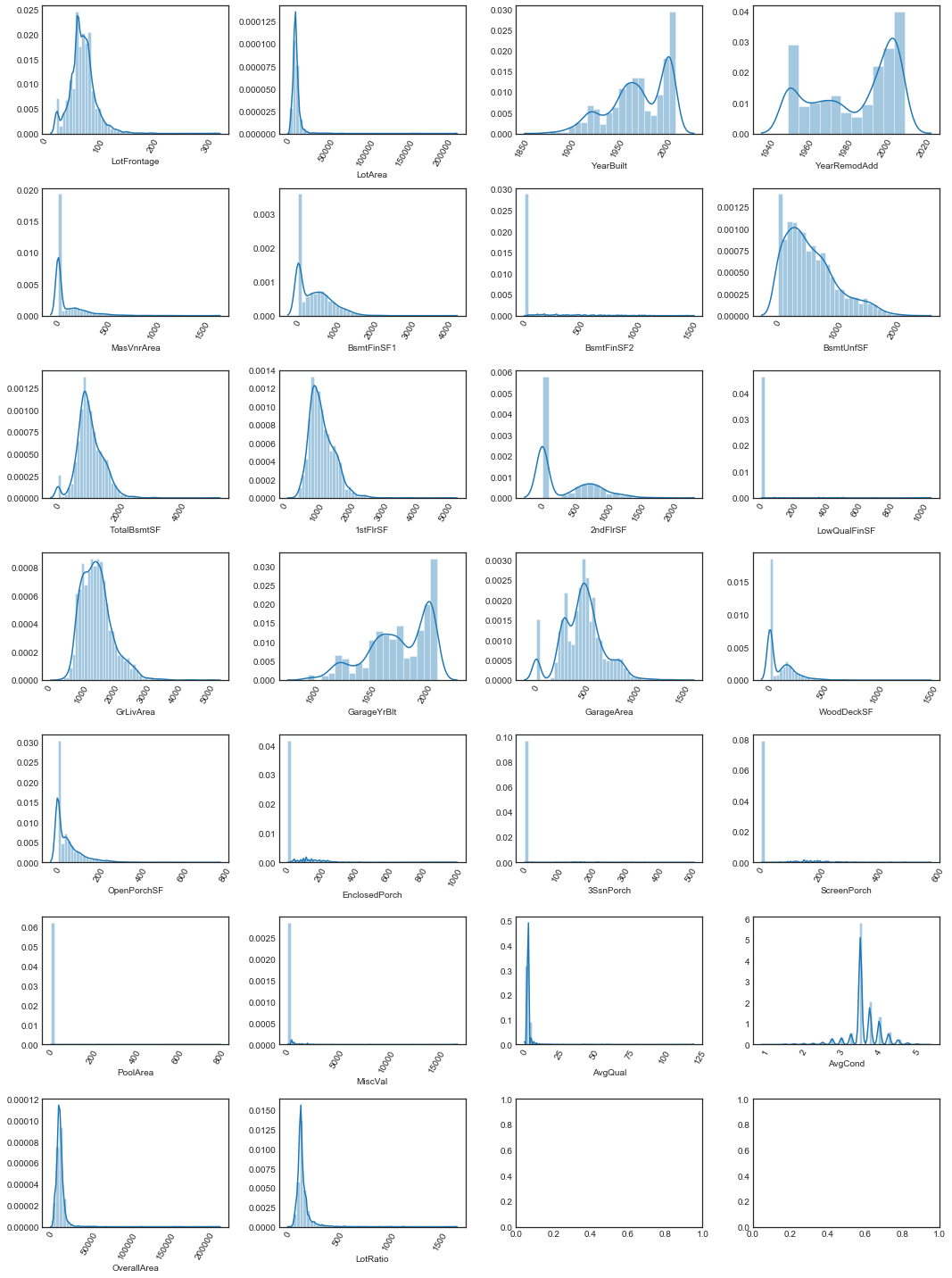

# inspect distributions of quantitatives including new ones

plot_cont_dists(nrows=7, ncols=4, data=quants_data.drop(columns=['SalePrice']), figsize=(15, 20))

# find minimum value over all quantitatives

quants_min_nonzero = quants_data[quants_data != 0].min().min()

print(f"Minimum quantitative value is {quants_data.min().min()}")

print(f"Minimum nonzero quantitative value is {quants_min_nonzero}")

Minimum quantitative value is 0.0

Minimum nonzero quantitative value is 0.4444444444444444

Since the minimum nonzero quantitative value is , we must set (quants_min) if in order not to interfere with monotonicity

# Columns to log transform

log_cols = quants_data.columns.drop(['YearBuilt', 'YearRemodAdd', 'GarageYrBlt', 'GarageArea', 'AvgCond'])

log_cols

Index(['LotFrontage', 'LotArea', 'MasVnrArea', 'BsmtFinSF1', 'BsmtFinSF2',

'BsmtUnfSF', 'TotalBsmtSF', '1stFlrSF', '2ndFlrSF', 'LowQualFinSF',

'GrLivArea', 'WoodDeckSF', 'OpenPorchSF', 'EnclosedPorch', '3SsnPorch',

'ScreenPorch', 'PoolArea', 'MiscVal', 'SalePrice', 'AvgQual',

'OverallArea', 'LotRatio'],

dtype='object')

# log transform SalePrice

clean.data = log_transform(data=clean.data, log_cols=['SalePrice'])

drop.data = log_transform(data=drop.data, log_cols=['SalePrice'])

# log transform most quantitatives

clean_edit.data = log_transform(data=clean_edit.data, log_cols=log_cols)

drop_edit.data = log_transform(data=drop_edit.data, log_cols=log_cols)

Model selection and tuning

Create modeling datasets

# set col kinds attribute of HPDataFramePlus attribute for model data method

do_col_kinds(drop)

do_col_kinds(drop_edit)

do_col_kinds(clean)

do_col_kinds(clean_edit)

# model data

mclean = HPDataFramePlus(data=clean.get_model_data(response='log_SalePrice'))

mclean_edit = HPDataFramePlus(data=clean_edit.get_model_data(response='log_SalePrice'))

mdrop = HPDataFramePlus(data=drop.get_model_data(response='log_SalePrice'))

mdrop_edit = HPDataFramePlus(data=drop_edit.get_model_data(response='log_SalePrice'))

mclean.data.info()

<class 'pandas.core.frame.DataFrame'>

MultiIndex: 2916 entries, (train, 1) to (test, 2919)

Columns: 230 entries, LotFrontage to log_SalePrice

dtypes: float64(230)

memory usage: 5.2+ MB

mclean_edit.data.info()

<class 'pandas.core.frame.DataFrame'>

MultiIndex: 2916 entries, (train, 1) to (test, 2919)

Columns: 222 entries, LotShape to log_SalePrice

dtypes: float64(222)

memory usage: 5.0+ MB

mdrop.data.info()

<class 'pandas.core.frame.DataFrame'>

MultiIndex: 2916 entries, (train, 1) to (test, 2919)

Columns: 173 entries, LotFrontage to log_SalePrice

dtypes: float64(173)

memory usage: 4.0+ MB

mdrop_edit.data.info()

<class 'pandas.core.frame.DataFrame'>

MultiIndex: 2916 entries, (train, 1) to (test, 2919)

Columns: 176 entries, LotShape to log_SalePrice

dtypes: float64(176)

memory usage: 4.0+ MB

Compare default models for baseline

hpdfs = [mclean, mdrop, mclean_edit, mdrop_edit]

data_names = ['clean', 'drop', 'clean_edit', 'drop_edit']

response = 'log_SalePrice'

model_data = build_model_data(hpdfs, data_names, response)

First we’ll look at a selection of untuned models with default parameters to get a rough idea of which ones might have better performance.

We’ll use root mean squared error (RMSE) for our loss function. Since we have a relatively small dataset, we’ll use cross-validation to estimate rmse for test data.

# fit some default regressor models

def_models = {'lasso': Lasso(),

'ridge': Ridge(),

'bridge': BayesianRidge(),

'pls': PLSRegression(),

'svr': SVR(),

'knn': KNeighborsRegressor(),

'mlp': MLPRegressor(),

'dectree': DecisionTreeRegressor(random_state=27),

'extratree': ExtraTreeRegressor(random_state=27),

'xgb': XGBRegressor(objective='reg:squarederror', random_state=27, n_jobs=-1)}

fit_def_models = fit_default_models(model_data, def_models)

# compare default models

def_comp_df = compare_performance(fit_def_models, model_data, random_state=27)

def_comp_df.sort_values(by=('clean', 'cv_rmse')).reset_index(drop=True)

| data | model | clean | drop | clean_edit | drop_edit | ||||

|---|---|---|---|---|---|---|---|---|---|

| performance | train_rmse | cv_rmse | train_rmse | cv_rmse | train_rmse | cv_rmse | train_rmse | cv_rmse | |

| 0 | bridge | 0.0950012 | 0.115226 | 0.0988284 | 0.11371 | 0.094478 | 0.11409 | 0.0996576 | 0.115962 |

| 1 | ridge | 0.0948572 | 0.116246 | 0.099311 | 0.114194 | 0.094225 | 0.113706 | 0.0998434 | 0.116375 |

| 2 | xgb | 0.0853461 | 0.122093 | 0.0895599 | 0.123479 | 0.0876669 | 0.123595 | 0.0889219 | 0.126636 |

| 3 | pls | 0.122064 | 0.127405 | 0.127452 | 0.133998 | 0.130416 | 0.13708 | 0.133912 | 0.139404 |

| 4 | svr | 0.122741 | 0.134491 | 0.123251 | 0.13529 | 0.120197 | 0.131894 | 0.123082 | 0.134709 |

| 5 | mlp | 0.116434 | 0.172462 | 0.123199 | 0.182601 | 0.113073 | 0.162779 | 0.122168 | 0.171919 |

| 6 | dectree | 2.93011e-05 | 0.200113 | 2.52372e-05 | 0.205864 | 3.15449e-05 | 0.206949 | 2.48969e-05 | 0.200551 |

| 7 | knn | 0.164677 | 0.20921 | 0.161079 | 0.201135 | 0.153413 | 0.194985 | 0.153466 | 0.18835 |

| 8 | extratree | 2.26808e-05 | 0.211913 | 1.40429e-05 | 0.216413 | 1.66016e-05 | 0.209181 | 1.87349e-05 | 0.213926 |

| 9 | lasso | 0.399557 | 0.399865 | 0.399557 | 0.399721 | 0.399557 | 0.400058 | 0.399557 | 0.399743 |

# compare train and cv performance for each dataset

data_palette = {'train_rmse': 'cornflowerblue', 'cv_rmse': 'midnightblue'}

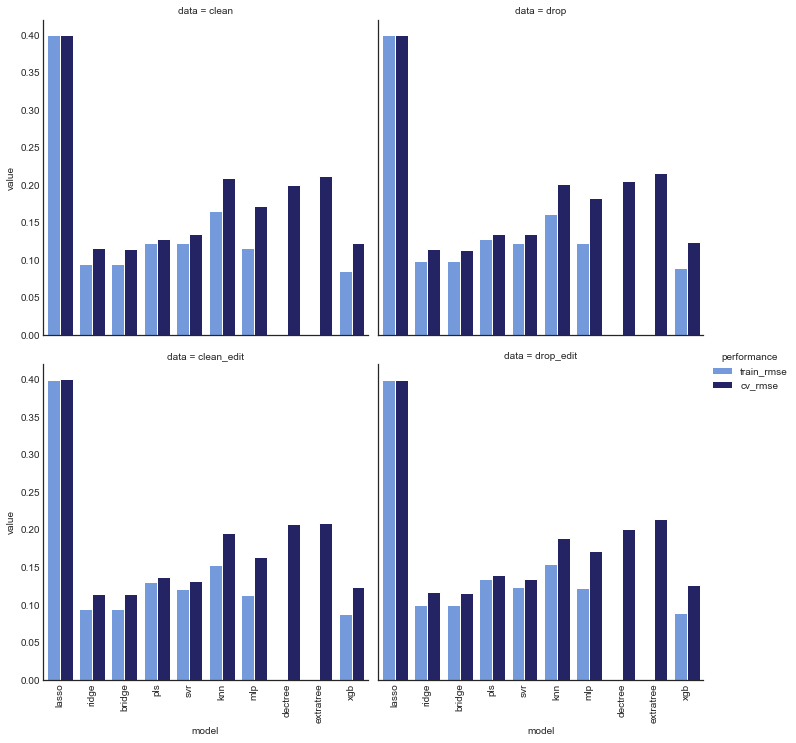

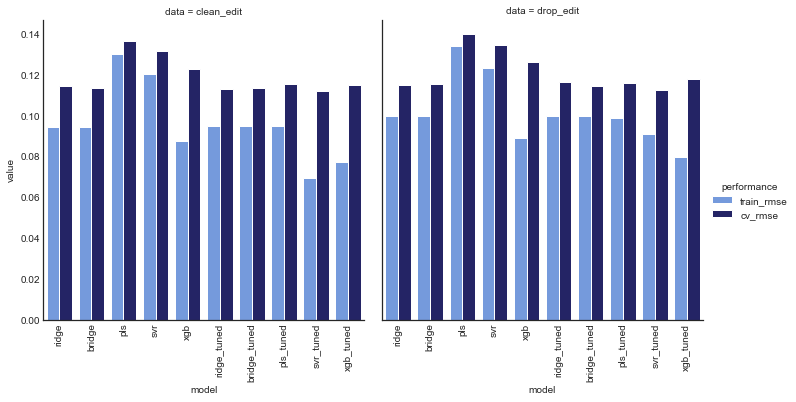

plot_model_comp(def_comp_df, col='data', hue='performance', kind='bar',

palette=data_palette, col_wrap=2)

Unsurprisingly, all models (with the exception of lasso regression) had worse CV error than train error. However, for some models the difference was much greater, and these are likely overfitting. In particular, dectree, extratree had cv error roughly 5 orders of magnitude greater than train error, and mlp, knn, and xgb also saw significant increases.

The other models (ridge, bridge, pls and svr) saw slighter differences in cv and train errors, and are thus less likely overfitting.

# compare train and cv error across datasets

perf_palette = {'drop': 'midnightblue', 'clean': 'forestgreen', 'drop_edit': 'crimson',

'clean_edit': 'darkorange'}

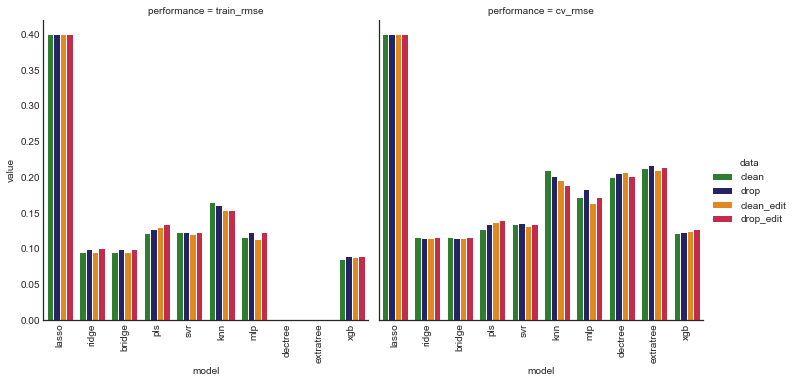

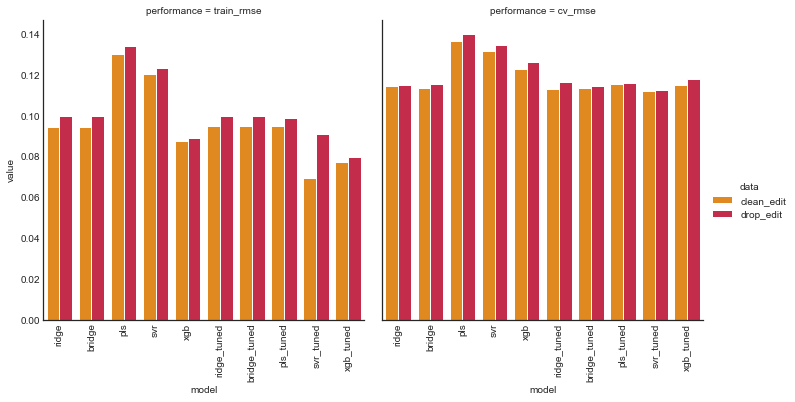

plot_model_comp(def_comp_df, col='performance', hue='data', kind='bar',

palette=perf_palette)

Based on cv rmse, the most promising models appear to be ridge, bridge, xgb, svr, and pls, which are ridge, Bayesian ridge, gradient boosted decision tree, support vector and partial least squared regressors, respectively.

drop_cols = [(data_name, 'train_rmse') for data_name in data_names]

def_comp_cv = def_comp_df.drop(columns=drop_cols).sort_values(by=('clean', 'cv_rmse'))

def_comp_cv

| data | model | clean | drop | clean_edit | drop_edit |

|---|---|---|---|---|---|

| performance | cv_rmse | cv_rmse | cv_rmse | cv_rmse | |

| 2 | bridge | 0.115226 | 0.11371 | 0.11409 | 0.115962 |

| 1 | ridge | 0.116246 | 0.114194 | 0.113706 | 0.116375 |

| 9 | xgb | 0.122093 | 0.123479 | 0.123595 | 0.126636 |

| 3 | pls | 0.127405 | 0.133998 | 0.13708 | 0.139404 |

| 4 | svr | 0.134491 | 0.13529 | 0.131894 | 0.134709 |

| 6 | mlp | 0.172462 | 0.182601 | 0.162779 | 0.171919 |

| 7 | dectree | 0.200113 | 0.205864 | 0.206949 | 0.200551 |

| 5 | knn | 0.20921 | 0.201135 | 0.194985 | 0.18835 |

| 8 | extratree | 0.211913 | 0.216413 | 0.209181 | 0.213926 |

| 0 | lasso | 0.399865 | 0.399721 | 0.400058 | 0.399743 |

Almost all models had an improvement in cv rmse when features were added, so it appears the feature engineering was warranted.

# top models by cv performance for each data set

rank_models_on_data(def_comp_cv, model_data)

| data | model | clean | drop | clean_edit | drop_edit |

|---|---|---|---|---|---|

| performance | cv_rmse | cv_rmse | cv_rmse | cv_rmse | |

| 2 | bridge | 1 | 1 | 2 | 1 |

| 1 | ridge | 2 | 2 | 1 | 2 |

| 9 | xgb | 3 | 3 | 3 | 3 |

| 3 | pls | 4 | 4 | 5 | 5 |

| 4 | svr | 5 | 5 | 4 | 4 |

| 6 | mlp | 6 | 6 | 6 | 6 |

| 7 | dectree | 7 | 8 | 8 | 8 |

| 5 | knn | 8 | 7 | 7 | 7 |

| 8 | extratree | 9 | 9 | 9 | 9 |

| 0 | lasso | 10 | 10 | 10 | 10 |

The top five models were consistent across all four versions of the dataset, and were the promising models identified earlier. In order, they are ridge, bridge, xgb, with svr and pls tied for fourth.

# rank model performance across data sets

rank_models_across_data(def_comp_cv, model_data)

| data | model | clean | drop | clean_edit | drop_edit |

|---|---|---|---|---|---|

| performance | cv_rmse | cv_rmse | cv_rmse | cv_rmse | |

| 2 | bridge | 3 | 1 | 2 | 4 |

| 1 | ridge | 3 | 2 | 1 | 4 |

| 9 | xgb | 1 | 2 | 3 | 4 |

| 3 | pls | 1 | 2 | 3 | 4 |

| 4 | svr | 2 | 4 | 1 | 3 |

| 6 | mlp | 3 | 4 | 1 | 2 |

| 7 | dectree | 1 | 3 | 4 | 2 |

| 5 | knn | 4 | 3 | 2 | 1 |

| 8 | extratree | 2 | 4 | 1 | 3 |

| 0 | lasso | 3 | 1 | 4 | 2 |

The top model, ridge performed best on clean_edit and drop_edit. The next best model, bridge performed best on clean and clean_edit. Third and fourth xgb and pls performed best on clean and drop. Finally svr performed best on clean_edit and drop_edit.

Tune best individual models

Here we’ll focus on tuning the most promising models from the last section. We’ll use both clean_edit and drop_edit since the top model performed best on these.

# retain top 5 models

drop_models = ['lasso', 'dectree', 'extratree', 'knn', 'mlp']

models = remove_models(fit_def_models, drop_models)

try:

# drop models for clean and drop data

models.pop('clean')

models.pop('drop')

# drop clean and drop data

model_data.pop('clean')

model_data.pop('drop')

except KeyError:

pass

print(f'Promising models are {list(models["clean_edit"].keys())}')

Promising models are ['ridge', 'bridge', 'pls', 'svr', 'xgb']

# train test input output for clean_edit (y_test values are NaN)

X_ce_train = model_data['clean_edit']['X_clean_edit_train']

X_ce_test = model_data['clean_edit']['X_clean_edit_test']

y_ce_train = model_data['clean_edit']['y_clean_edit_train']

# train test input output for clean_edit (y_test values are NaN)

X_de_train = model_data['drop_edit']['X_drop_edit_train']

X_de_test = model_data['drop_edit']['X_drop_edit_test']

y_de_train = model_data['drop_edit']['y_drop_edit_train']

Ridge regression

Ridge regression is linear least squares with an regularization term. We’ll fit default ridge regression models and then tune for comparison.

# Default ridge regression models

ridge_models = defaultdict(dict)

ridge_models['clean_edit']['ridge_def'] = Ridge().fit(X_ce_train, y_ce_train)

ridge_models['drop_edit']['ridge_def'] = Ridge().fit(X_de_train, y_de_train)

Bayesian hyperparameter optimization is an efficient tuning method. We’ll optimize with respect to cv rmse

# ridge regression hyperparameters search space

ridge_space = {'alpha': hp.loguniform('alpha', low=-3*np.log(10), high=2*np.log(10))}

# container for hyperparameter search trials and results

model_ho_results = defaultdict(dict)

# store trial objects for restarting training

model_ho_results['clean_edit']['ridge_tuned'] = {'trials': Trials(), 'params': None}

model_ho_results['drop_edit']['ridge_tuned'] = {'trials': Trials(), 'params': None}

# optimize hyperparameters

model_ho_results['clean_edit']['ridge_tuned'] = \

ho_results(obj=ho_cv_rmse, space=ridge_space,

est_name='ridge', X_train=X_ce_train,

y_train=y_ce_train,

max_evals=100, random_state=27,

trials=model_ho_results['clean_edit']['ridge_tuned']['trials'])

model_ho_results['drop_edit']['ridge_tuned'] = \

ho_results(obj=ho_cv_rmse, space=ridge_space,

est_name='ridge', X_train=X_de_train,

y_train=y_de_train,

max_evals=100, random_state=27,

trials=model_ho_results['drop_edit']['ridge_tuned']['trials'])

100%|██████████| 100/100 [00:08<00:00, 11.38it/s, best loss: 0.11253072830975036]

100%|██████████| 100/100 [00:07<00:00, 13.32it/s, best loss: 0.11564439386901282]

%%capture

# create and fit models with optimal hyperparameters

ridge_models['clean_edit']['ridge_tuned'] = \

Ridge(**model_ho_results['clean_edit']['ridge_tuned']['params'])

ridge_models['drop_edit']['ridge_tuned'] = \

Ridge(**model_ho_results['drop_edit']['ridge_tuned']['params'])

ridge_models['clean_edit']['ridge_tuned'].fit(X_ce_train, y_ce_train)

ridge_models['drop_edit']['ridge_tuned'].fit(X_de_train, y_de_train)

# compare Ridge regression models

compare_performance(ridge_models, model_data, random_state=27)

| data | model | clean_edit | drop_edit | ||

|---|---|---|---|---|---|

| performance | train_rmse | cv_rmse | train_rmse | cv_rmse | |

| 0 | ridge_def | 0.094225 | 0.11256 | 0.0998434 | 0.115635 |

| 1 | ridge_tuned | 0.0950445 | 0.11315 | 0.0996629 | 0.114869 |

The ridge regression model trained on the clean_edit dataset and tuned with Bayesian search had the best cv rmse. We note however that the model trained on drop_edit had a , which is promising (a lower train rmse might indicate overfitting).

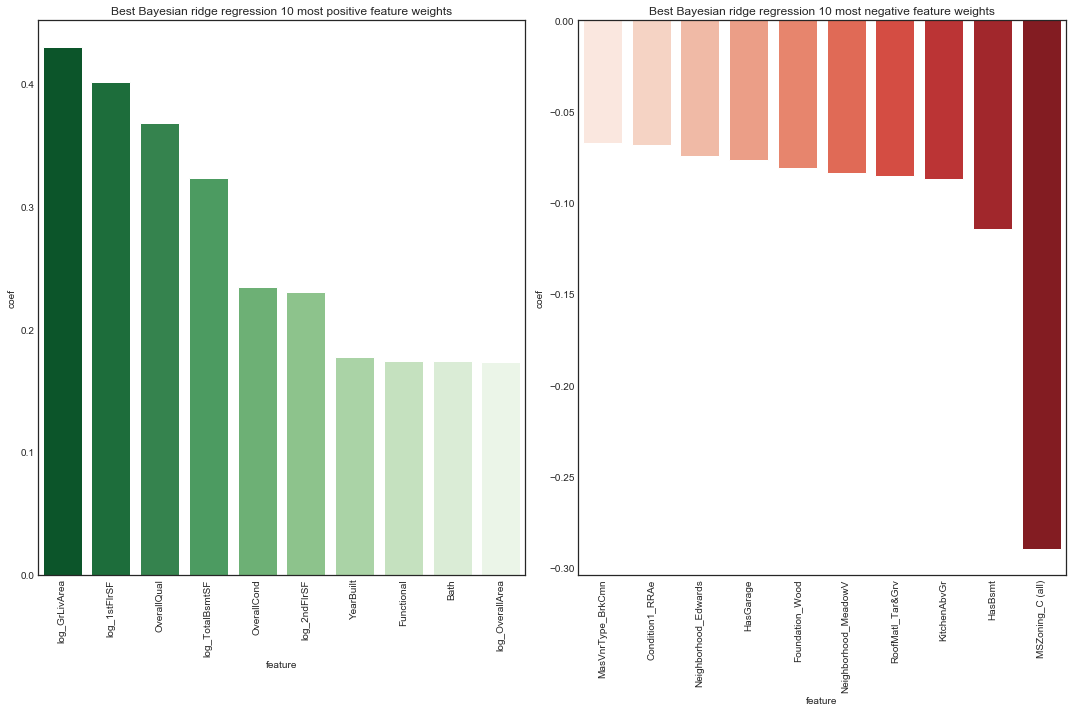

Since ridge regression is just linear regression with a regularization term, it’s relatively straightfoward to interpret. We’ll rank the features of the best model their coefficient weights.

# Top and bottom 10 features in best ridge model

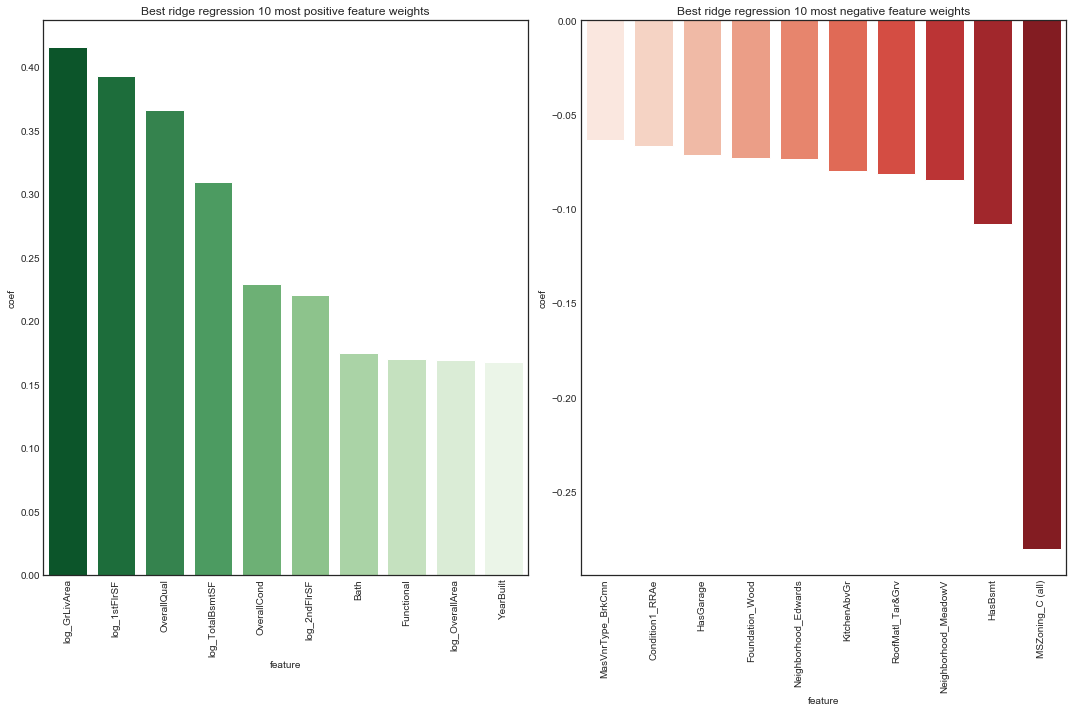

plot_features(ridge_models['clean_edit']['ridge_tuned'], 'ridge regression', X_ce_train, 10,

figsize=(15, 10), rotation=90)

The rankings of most positive feature weights are not too suprising. The most postively weighted feature was overall quality. We note condition variables and size variables are prominent.

The rankings of most negative feature weights are perhaps more surprising, in particular the presence of a basement and number of kitchens. Interestingly, several neighborhoods stand out as having a negative association with sale price. The most negatively weighted feature was the property being zoned commercial.

# add tuned ridge models

models['clean_edit']['ridge_tuned'] = ridge_models['clean_edit']['ridge_tuned']

models['drop_edit']['ridge_tuned'] = ridge_models['drop_edit']['ridge_tuned']

Bayesian Ridge regression

Bayesian ridge regression is similar to ridge regression except it uses Bayesian methods to estimate the regularization parameter from the data.

# Default Bayesian Ridge models

bridge_models = defaultdict(dict)

bridge_models['clean_edit']['bridge_def'] = BayesianRidge().fit(X_ce_train, y_ce_train)

bridge_models['drop_edit']['bridge_def'] = BayesianRidge().fit(X_de_train, y_de_train)

# bayesian ridge regression hyperparameter space

bridge_space = {'alpha_1': hp.loguniform('alpha_1', low=-9*np.log(10), high=3*np.log(10)),

'alpha_2': hp.loguniform('alpha_2', low=-9*np.log(10), high=3*np.log(10)),

'lambda_1': hp.loguniform('lambda_1', low=-9*np.log(10), high=3*np.log(10)),

'lambda_2': hp.loguniform('lambda_2', low=-9*np.log(10), high=3*np.log(10))}

# store trial objects for restarting training

model_ho_results['clean_edit']['bridge_tuned'] = {'trials': Trials(), 'params': None}

model_ho_results['drop_edit']['bridge_tuned'] = {'trials': Trials(), 'params': None}

# optimize hyperparameters

model_ho_results['clean_edit']['bridge_tuned'] = \

ho_results(obj=ho_cv_rmse, space=bridge_space,

est_name='bridge', X_train=X_ce_train,

y_train=y_ce_train,

max_evals=100, random_state=27,

trials=model_ho_results['clean_edit']['bridge_tuned']['trials'])

model_ho_results['drop_edit']['bridge_tuned'] = \

ho_results(obj=ho_cv_rmse, space=bridge_space,

est_name='bridge', X_train=X_de_train,

y_train=y_de_train,

max_evals=100, random_state=27,

trials=model_ho_results['drop_edit']['bridge_tuned']['trials'])

100%|██████████| 100/100 [00:37<00:00, 2.67it/s, best loss: 0.11254203419476108]

100%|██████████| 100/100 [00:27<00:00, 3.66it/s, best loss: 0.11576647439940951]

%%capture

# add and fit models with optimal hyperparameters

bridge_models['clean_edit']['bridge_tuned'] = \

BayesianRidge(**model_ho_results['clean_edit']['bridge_tuned']['params'])

bridge_models['drop_edit']['bridge_tuned'] = \

BayesianRidge(**model_ho_results['drop_edit']['bridge_tuned']['params'])

bridge_models['clean_edit']['bridge_tuned'].fit(X_ce_train, y_ce_train)

bridge_models['drop_edit']['bridge_tuned'].fit(X_de_train, y_de_train)

# compare Ridge regression models

compare_performance(bridge_models, model_data, random_state=27)

| data | model | clean_edit | drop_edit | ||

|---|---|---|---|---|---|

| performance | train_rmse | cv_rmse | train_rmse | cv_rmse | |

| 0 | bridge_def | 0.094478 | 0.113612 | 0.0996576 | 0.114887 |

| 1 | bridge_tuned | 0.09467 | 0.114397 | 0.0996135 | 0.115072 |

As with ordinary ridge regression, the Bayesian ridge model trained on the clean_edit data and tuned with Bayesian search had the best cv rmse.

As with ridge regression, the model is straightforward to interpret.

# Top and bottom 10 features in best Bayesian ridge model

plot_features(bridge_models['clean_edit']['bridge_tuned'], 'Bayesian ridge regression', X_ce_train, 10,

figsize=(15, 10), rotation=90)

Feature weight rankings are nearly identical to the ridge model.

# add tuned bridge models

models['clean_edit']['bridge_tuned'] = bridge_models['clean_edit']['bridge_tuned']

models['drop_edit']['bridge_tuned'] = bridge_models['drop_edit']['bridge_tuned']

Partial Least Squares

Partial least squares regression stands out among the other models we’re tuning here as the only dimensional reduction method. It is well-suited to multicollinearity in the input data.

# Default partial least squares models

pls_models = defaultdict(dict)

pls_models['clean_edit']['pls_def'] = PLSRegression().fit(X_ce_train, y_ce_train)

pls_models['drop_edit']['pls_def'] = PLSRegression().fit(X_de_train, y_de_train)

The main hyperparameter of interest in partial least squared is the number of components (analogous to the number of components in principal component analysis) which is essentially the number of dimensions of the reduced dataset.

# partial least squares hyperparameter spaces

pls_ce_space = {'max_iter': ho_scope.int(hp.quniform('max_iter', low=200,

high=10000, q=10)),

'n_components': ho_scope.int(hp.quniform('n_components', low=2,

high=X_ce_train.shape[1] - 2, q=1))

}

pls_de_space = {'max_iter': ho_scope.int(hp.quniform('max_iter', low=200,

high=10000, q=10)),

'n_components': ho_scope.int(hp.quniform('n_components', low=2,

high=X_de_train.shape[1] - 2, q=1))}

# store trial objects for restarting training

model_ho_results['clean_edit']['pls_tuned'] = {'trials': Trials(), 'params': None}

model_ho_results['drop_edit']['pls_tuned'] = {'trials': Trials(), 'params': None}

# optimize hyperparameters

model_ho_results['clean_edit']['pls_tuned'] = \

ho_results(obj=ho_cv_rmse, space=pls_ce_space, est_name='pls',

X_train=X_ce_train, y_train=y_ce_train, max_evals=100,

random_state=27,

trials=model_ho_results['clean_edit']['pls_tuned']['trials'])

model_ho_results['drop_edit']['pls_tuned'] = \

ho_results(obj=ho_cv_rmse, space=pls_de_space, est_name='pls',

X_train=X_de_train, y_train=y_de_train, max_evals=100,

random_state=27,

trials=model_ho_results['drop_edit']['pls_tuned']['trials'])

100%|██████████| 100/100 [01:30<00:00, 1.11it/s, best loss: 0.11628329440486904]

100%|██████████| 100/100 [01:02<00:00, 1.60it/s, best loss: 0.11672287624670073]

%%capture

# workaround to cast results of hyperopt param search to correct type

conv_params = ['max_iter', 'n_components']

model_ho_results['clean_edit']['pls_tuned']['params'] = \

convert_to_int(model_ho_results['clean_edit']['pls_tuned']['params'],

conv_params)

model_ho_results['drop_edit']['pls_tuned']['params'] = \

convert_to_int(model_ho_results['drop_edit']['pls_tuned']['params'],

conv_params)

# add and fit models with optimal hyperparameters

pls_models['clean_edit']['pls_tuned'] = \

PLSRegression(**model_ho_results['clean_edit']['pls_tuned']['params'])

pls_models['drop_edit']['pls_tuned'] = \

PLSRegression(**model_ho_results['drop_edit']['pls_tuned']['params'])

pls_models['clean_edit']['pls_tuned'].fit(X_ce_train, y_ce_train)

pls_models['drop_edit']['pls_tuned'].fit(X_de_train, y_de_train)

# inspect pls optimal parameters

print(f"On the clean_edit data, optimal PLS parameters are: \n\t {model_ho_results['clean_edit']['pls_tuned']['params']}")

print(f"On the drop_edit data, optimal PLS parameters are: \n\t {model_ho_results['drop_edit']['pls_tuned']['params']}")

On the clean_edit data, optimal PLS parameters are:

{'max_iter': 5690, 'n_components': 12}

On the drop_edit data, optimal PLS parameters are:

{'max_iter': 2640, 'n_components': 16}

Interestingly, only a small number of components were deemed optimal! It’s worth recalling that this likely reflects a local minimum in the loss function, so the result should be taken with a grain of salt. However, it is interesting to note that such a low number of components are sufficient to get a competitive model.

# compare Bayesian Ridge models on clean and edit datasets

compare_performance(pls_models, model_data)

| data | model | clean_edit | drop_edit | ||

|---|---|---|---|---|---|

| performance | train_rmse | cv_rmse | train_rmse | cv_rmse | |

| 0 | pls_def | 0.130416 | 0.136774 | 0.133912 | 0.139224 |

| 1 | pls_tuned | 0.0948243 | 0.115228 | 0.0989862 | 0.116016 |

In contrast to ridge and Bayesian ridge regression, the tuned partial least squares had slightly lower cv rmse on the drop_edit dataset. This cv rmse is very close to that of tuned ridge and Bayesian ridge models – it’s remarkable that only 16 components are required!

# add tuned pls models

models['clean_edit']['pls_tuned'] = pls_models['clean_edit']['pls_tuned']

models['drop_edit']['pls_tuned'] = pls_models['drop_edit']['pls_tuned']

Support Vector Machine

# Default support vector models

svr_models = defaultdict(dict)

svr_models['clean_edit']['svr_def'] = SVR().fit(X_ce_train, y_ce_train)

svr_models['drop_edit']['svr_def'] = SVR().fit(X_de_train, y_de_train)

# hyperparameter space for SVR with rbf kernel

svr_space = {'gamma': hp.loguniform('gamma', low=-3*np.log(10), high=2*np.log(10)),

'C': hp.loguniform('C', low=-3*np.log(10), high=2*np.log(10)),

'epsilon': hp.loguniform('epsilon', low=-3*np.log(10), high=2*np.log(10))

}

# store trial objects for restarting training

model_ho_results['clean_edit']['svr_tuned'] = {'trials': Trials(), 'params': None}

model_ho_results['drop_edit']['svr_tuned'] = {'trials': Trials(), 'params': None}

# optimize hyperparameters

model_ho_results['clean_edit']['svr_tuned'] = \

ho_results(obj=ho_cv_rmse, space=svr_space, est_name='svr',

X_train=X_ce_train, y_train=y_ce_train, max_evals=50,

random_state=27,

trials=model_ho_results['clean_edit']['svr_tuned']['trials'])

model_ho_results['drop_edit']['svr_tuned'] = \

ho_results(obj=ho_cv_rmse, space=svr_space, est_name='svr',

X_train=X_de_train, y_train=y_de_train, max_evals=50,

random_state=27,

trials=model_ho_results['drop_edit']['svr_tuned']['trials'])

100%|██████████| 50/50 [01:37<00:00, 1.95s/it, best loss: 0.11318101455546818]

100%|██████████| 50/50 [01:32<00:00, 1.84s/it, best loss: 0.11424890264814005]

%%capture

# fit models with optimal hyperparameters

svr_models['clean_edit']['svr_tuned'] = \

SVR(**model_ho_results['clean_edit']['svr_tuned']['params'])

svr_models['drop_edit']['svr_tuned'] = \

SVR(**model_ho_results['drop_edit']['svr_tuned']['params'])

svr_models['clean_edit']['svr_tuned'].fit(X_ce_train, y_ce_train)

svr_models['drop_edit']['svr_tuned'].fit(X_de_train, y_de_train)

# compare SVR model performance on clean and edit datasets

svr_comp_df = compare_performance(svr_models, model_data)

svr_comp_df

As with all previous models, we’re seeing better performance on drop_edit. Again, a higher train rmse on drop_edit but a lower cv rmse is a positive sign.

# add tuned svr models

models['clean_edit']['svr_tuned'] = svr_models['clean_edit']['svr_tuned']

models['drop_edit']['svr_tuned'] = svr_models['drop_edit']['svr_tuned']

Gradient boosted trees

# Default gradient boost tree models

xgb_models = defaultdict(dict)

xgb_models['clean_edit']['xgb_def'] = XGBRegressor(objective='reg:squarederror', random_state=27, n_jobs=-1)

xgb_models['drop_edit']['xgb_def'] = XGBRegressor(objective='reg:squarederror', random_state=27, n_jobs=-1)

xgb_models['clean_edit']['xgb_def'].fit(X_ce_train.values, y_ce_train.values)

xgb_models['drop_edit']['xgb_def'].fit(X_de_train.values, y_de_train.values)

XGBRegressor(base_score=0.5, booster='gbtree', colsample_bylevel=1,

colsample_bynode=1, colsample_bytree=1, gamma=0,

importance_type='gain', learning_rate=0.1, max_delta_step=0,

max_depth=3, min_child_weight=1, missing=None, n_estimators=100,

n_jobs=-1, nthread=None, objective='reg:squarederror',

random_state=27, reg_alpha=0, reg_lambda=1, scale_pos_weight=1,

seed=None, silent=None, subsample=1, verbosity=1)

# hyperparameter spaces

xgb_space = {'max_depth': ho_scope.int(hp.quniform('max_depth', low=1, high=3, q=1)),

'n_estimators': ho_scope.int(hp.quniform('n_estimators', low=100, high=500, q=50)),

'learning_rate': hp.loguniform('learning_rate', low=-4*np.log(10), high=0),

'gamma': hp.loguniform('gamma', low=-3*np.log(10), high=2*np.log(10)),

'min_child_weight': ho_scope.int(hp.quniform('min_child_weight', low=1, high=7, q=1)),

'subsample': hp.uniform('subsample', low=0.25, high=1),

'colsample_bytree': hp.uniform('colsample_bytree', low=0.25, high=1),

'colsample_bylevel': hp.uniform('colsample_bylevel', low=0.25, high=1),

'colsample_bynode': hp.uniform('colsample_bynode', low=0.25, high=1),

'reg_lambda': hp.loguniform('reg_lambda', low=-2*np.log(10), high=2*np.log(10)),

'reg_alpha': hp.loguniform('reg_alpha', low=-1*np.log(10), high=1*np.log(10)),

}

# store trial objects for restarting training

model_ho_results['clean_edit']['xgb_tuned'] = {'trials': Trials(), 'params': None}

model_ho_results['drop_edit']['xgb_tuned'] = {'trials': Trials(), 'params': None}

# optimize hyperparameters

model_ho_results['clean_edit']['xgb_tuned'] = \

ho_results(obj=ho_cv_rmse, space=xgb_space, est_name='xgb',

X_train=X_ce_train, y_train=y_ce_train, max_evals=50,

random_state=27,

trials=model_ho_results['clean_edit']['xgb_tuned']['trials'])

model_ho_results['drop_edit']['xgb_tuned'] = \

ho_results(obj=ho_cv_rmse, space=xgb_space, est_name='xgb',

X_train=X_de_train, y_train=y_de_train, max_evals=50,

random_state=27,

trials=model_ho_results['drop_edit']['xgb_tuned']['trials'])

100%|██████████| 50/50 [09:51<00:00, 11.82s/it, best loss: 0.11487854997487522]

100%|██████████| 50/50 [08:56<00:00, 10.74s/it, best loss: 0.12018590987034897]

%%capture

# convert params to int

conv_params = ['max_depth', 'min_child_weight', 'n_estimators']

model_ho_results['clean_edit']['xgb_tuned']['params'] = \

convert_to_int(model_ho_results['clean_edit']['xgb_tuned']['params'], conv_params)

model_ho_results['clean_edit']['xgb_tuned']['params'] = \

convert_to_int(model_ho_results['clean_edit']['xgb_tuned']['params'], conv_params)

# add and fit models with optimal hyperparameters

fixed_params = {'objective': 'reg:squarederror', 'n_jobs': -1, 'random_state': 27}

xgb_models['clean_edit']['xgb_tuned'] = \

XGBRegressor(**{**model_ho_results['clean_edit']['xgb_tuned']['params'],

**fixed_params})

xgb_models['drop_edit']['xgb_tuned'] = \

XGBRegressor(**{**model_ho_results['clean_edit']['xgb_tuned']['params'],

**fixed_params})

xgb_models['clean_edit']['xgb_tuned'].fit(X_ce_train.values, y_ce_train.values)

xgb_models['drop_edit']['xgb_tuned'].fit(X_de_train.values, y_de_train.values)

# compare XGBoost models on clean_edit and drop_edit datasets

xgb_comp_df = compare_performance(xgb_models, model_data)

xgb_comp_df

| data | model | clean_edit | drop_edit | ||

|---|---|---|---|---|---|

| performance | train_rmse | cv_rmse | train_rmse | cv_rmse | |

| 0 | xgb_def | 0.0876669 | 0.125045 | 0.0889219 | 0.125903 |

| 1 | xgb_tuned | 0.0772716 | 0.113871 | 0.0795258 | 0.117488 |

In contrast to all previous models, the gradient boosted tree regressor had a lower cv rmse on clean_edit, but similarly to previous models train rmse was higher.

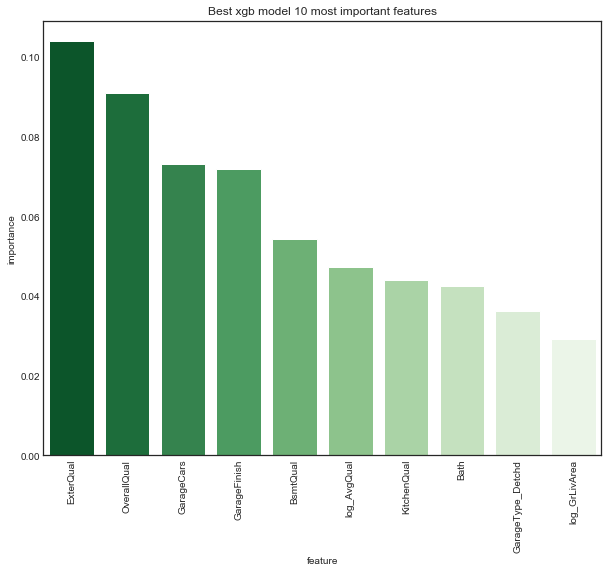

We can rank the features by importance (in this case, the number of times the feature was used to split a tree across all trees in the forest).

# top 20 feature importances of xgb model on drop_edit data

plot_xgb_features(xgb_models['drop_edit']['xgb_tuned'], X_de_train, 10, figsize=(10, 8),

rotation=90)

On the drop_edit data, the top ten features for the gradient boosted trees regression model seem quite different from the top ten features of ridge regression. Only OverallQual and log_GrLivArea appear in both, and whereas both rank OverallQual third, ridge ranks log_GrLivArea first while xgb ranks it tenth. While the top ridge features seemed plausible and natural, some of the top xgb features seem more surpising, especially the highest ranked feature GarageType_Detached.

# replace default models with tuned models

models['clean_edit']['xgb_tuned'] = xgb_models['clean_edit']['xgb_tuned']

models['drop_edit']['xgb_tuned'] = xgb_models['drop_edit']['xgb_tuned']

Compare tuned models and save parameters

# compare results of tuned models

tuned_comp_df = compare_performance(models, model_data, random_state=27)

tuned_comp_df.sort_values(by=('clean_edit', 'cv_rmse')).reset_index(drop=True)

| data | model | clean_edit | drop_edit | ||

|---|---|---|---|---|---|

| performance | train_rmse | cv_rmse | train_rmse | cv_rmse | |

| 0 | svr_tuned | 0.06929 | 0.112236 | 0.0911838 | 0.112445 |

| 1 | ridge_tuned | 0.0950445 | 0.113011 | 0.0996629 | 0.116393 |

| 2 | bridge_tuned | 0.09467 | 0.113658 | 0.0996135 | 0.114628 |

| 3 | bridge | 0.094478 | 0.113733 | 0.0996576 | 0.115385 |

| 4 | ridge | 0.094225 | 0.114597 | 0.0998434 | 0.11497 |

| 5 | xgb_tuned | 0.0772716 | 0.114933 | 0.0795258 | 0.11772 |

| 6 | pls_tuned | 0.0948243 | 0.115411 | 0.0989862 | 0.115752 |

| 7 | xgb | 0.0876669 | 0.123048 | 0.0889219 | 0.126444 |

| 8 | svr | 0.120197 | 0.131465 | 0.123082 | 0.134494 |

| 9 | pls | 0.130416 | 0.136702 | 0.133912 | 0.140016 |

# compare tuned model train and cv performance on clean and edit datasets

plot_model_comp(tuned_comp_df, col='data', hue='performance', kind='bar', palette=data_palette)

# compare clean and edit performance for train and cv error

plot_model_comp(tuned_comp_df, col='performance', hue='data', kind='bar', palette=perf_palette)

# pickle hyperopt trials and results

pickle_to_file(model_ho_results, '../training/model_tuning_results.pkl')

# pickle tuned models

pickle_to_file(models, '../training/tuned_models.pkl')

Ensembles

# unpickle tuned models from last section

tuned_models = pickle_from_file('../training/tuned_models.pkl')

Voting

Voting ensembles predict a weighted average of base models.

We’ll use the implementation sklearn.ensemble.VotingRegressor. Unfortunately sklearn.PLSRegressor’s predict method returns arrays of size (n_samples, 1) rather than (n_samples,) like all all other models. This throws an error when passed in as an estimator to cross_val_score so we won’t use it as a base model. We also won’t use bridge since its feature weights were nearly identical to ridge, so in the end our voting regressor will consist of three base models: ridge, support vector and gradient boosted tree regression.

tuned_models['clean_edit'].keys()

dict_keys(['ridge', 'bridge', 'pls', 'svr', 'xgb', 'ridge_tuned', 'bridge_tuned', 'pls_tuned', 'svr_tuned', 'xgb_tuned'])

drop_models = ['ridge', 'bridge', 'pls', 'svr', 'xgb', 'bridge_tuned',

'pls_tuned']

base_pretuned = remove_models(tuned_models, drop_models)

Default base and uniform weights

For a baseline, we’ll look at a voting ensemble of default base models with uniform weights

%%capture

# Default models for Voting Regressor

base_def = [('ridge', Ridge()),

('svr', SVR()),

('xgb', XGBRegressor(objective='reg:squarederror', n_jobs=-1, random_state=27))]

# Voting ensembles with uniform weights and untuned base models

ensembles = defaultdict(dict)

ensembles['clean_edit']['voter_def'] = VotingRegressor(base_def, n_jobs=-1)

ensembles['drop_edit']['voter_def'] = VotingRegressor(base_def, n_jobs=-1)

ensembles['clean_edit']['voter_def'].fit(X_ce_train.values, y_ce_train.values)

ensembles['drop_edit']['voter_def'].fit(X_de_train.values, y_de_train.values)

Pretuned base and uniform weights

We also consider a voting ensemble with pretuned base models and uniform weights.

%%capture

# Voting ensmebles with uniform weights for pretuned base models

ensembles['clean_edit']['voter_uniform_pretuned'] = \

VotingRegressor(list(base_pretuned['clean_edit'].items()), n_jobs=-1)

ensembles['drop_edit']['voter_uniform_pretuned'] = \

VotingRegressor(list(base_pretuned['drop_edit'].items()), n_jobs=-1)

ensembles['clean_edit']['voter_uniform_pretuned'].fit(X_ce_train.values, y_ce_train.values)

ensembles['drop_edit']['voter_uniform_pretuned'].fit(X_de_train.values, y_de_train.values)

# voting ensemble hyperparameters for pretuned base

weight_space = {'voter1': hp.uniform('voter1', low=0, high=1),

'voter2': hp.uniform('voter2', low=0, high=1),

'voter3': hp.uniform('voter3', low=0, high=1)

}

voter_fixed_params = {'n_jobs': -1}

# container for hyperparameter search trials and results

ens_ho_results = defaultdict(dict)

# store trial objects for restarting training

ens_ho_results['clean_edit']['voter_pretuned'] = {'trials': Trials(), 'params': None}

ens_ho_results['drop_edit']['voter_pretuned'] = {'trials': Trials(), 'params': None}

# optimize weights for voting ensemble with pretuned base

ens_ho_results['clean_edit']['voter_pretuned'] = \

ho_ens_results(obj=ho_ens_cv_rmse, space=weight_space, ens_name='voter',

base_ests=base_pretuned['clean_edit'],

X_train=X_ce_train, y_train=y_ce_train,

fixed_params=voter_fixed_params,

pretuned=True, random_state=27, max_evals=50,

trials=ens_ho_results['clean_edit']['voter_pretuned']['trials'])

ens_ho_results['drop_edit']['voter_pretuned'] = \

ho_ens_results(obj=ho_ens_cv_rmse, space=weight_space, ens_name='voter',

base_ests=base_pretuned['drop_edit'],

X_train=X_de_train, y_train=y_de_train,

fixed_params=voter_fixed_params,

pretuned=True, random_state=27, max_evals=50,

trials=ens_ho_results['drop_edit']['voter_pretuned']['trials'])

100%|██████████| 50/50 [16:35<00:00, 19.91s/it, best loss: 0.10821736452332247]

100%|██████████| 50/50 [12:22<00:00, 14.85s/it, best loss: 0.11169063598085288]

%%capture

# store and normalize weights

ce_pretuned_weights = list(ens_ho_results['clean_edit']['voter_pretuned']['params'].values())

de_pretuned_weights = list(ens_ho_results['drop_edit']['voter_pretuned']['params'].values())

ce_pretuned_weights = convert_and_normalize_weights(ce_pretuned_weights)

de_pretuned_weights = convert_and_normalize_weights(de_pretuned_weights)

# add and fit voting ensembles of pretuned base estimators with tuned weights

ensembles['clean_edit']['voter_pretuned'] = \

VotingRegressor(list(base_pretuned['clean_edit'].items()),

weights=ce_pretuned_weights)

ensembles['drop_edit']['voter_pretuned'] = \

VotingRegressor(list(base_pretuned['drop_edit'].items()),

weights=de_pretuned_weights)

ensembles['clean_edit']['voter_pretuned'].fit(X_ce_train.values, y_ce_train.values)

ensembles['drop_edit']['voter_pretuned'].fit(X_de_train.values, y_de_train.values)

Fully tuned voter

Finally, we’ll tune a voting regressors base model hyperparameters and voting weights simultaneously with Bayesian search.

# base hyperparameter spaces

ridge_base_space = {'alpha_ridge': hp.loguniform('alpha_ridge', low=-3*np.log(10), high=2*np.log(10))}

svr_base_space = {'gamma_svr': hp.loguniform('gamma_svr', low=-3*np.log(10), high=2*np.log(10)),

'C_svr': hp.loguniform('C_svr', low=-3*np.log(10), high=2*np.log(10)),

'epsilon_svr': hp.loguniform('epsilon_svr', low=-3*np.log(10), high=2*np.log(10))}

xgb_base_space = {'max_depth_xgb': ho_scope.int(hp.quniform('max_depth_xgb', low=1, high=3, q=1)),

'n_estimators_xgb': ho_scope.int(hp.quniform('n_estimators_xgb', low=100, high=500, q=50)),

'learning_rate_xgb': hp.loguniform('learning_rate_xgb', low=-4*np.log(10), high=0),

'gamma_xgb': hp.loguniform('gamma_xgb', low=-3*np.log(10), high=2*np.log(10)),

'min_child_weight_xgb': ho_scope.int(hp.quniform('min_child_weight_xgb', low=1, high=7, q=1)),

'subsample_xgb': hp.uniform('subsample_xgb', low=0.25, high=1),

'colsample_bytree_xgb': hp.uniform('colsample_bytree_xgb', low=0.25, high=1),

'colsample_bylevel_xgb': hp.uniform('colsample_bylevel_xgb', low=0.25, high=1),

'colsample_bynode_xgb': hp.uniform('colsample_bynode_xgb', low=0.25, high=1),

'reg_lambda_xgb': hp.loguniform('reg_lambda_xgb', low=-2*np.log(10), high=2*np.log(10)),

'reg_alpha_xgb': hp.loguniform('reg_alpha_xgb', low=-1*np.log(10), high=1*np.log(10)),

}

# voting ensemble hyperparameters for untuned base

base_space = {**ridge_base_space, **svr_base_space, **xgb_base_space}

voter_space = {**base_space, **weight_space}

# store trial objects for restarting training

ens_ho_results['clean_edit']['voter_tuned'] = {'trials': Trials(), 'params': None}

ens_ho_results['drop_edit']['voter_tuned'] = {'trials': Trials(), 'params': None}

# optimize all voting ensemble hyperparameters jointly

ens_ho_results['clean_edit']['voter_tuned'] = \

ho_ens_results(obj=ho_ens_cv_rmse, space=voter_space, ens_name='voter',

X_train=X_ce_train, y_train=y_ce_train,

fixed_params=voter_fixed_params,

pretuned=False, random_state=27, max_evals=50,

trials=ens_ho_results['clean_edit']['voter_tuned']['trials'])

ens_ho_results['drop_edit']['voter_tuned'] = \

ho_ens_results(obj=ho_ens_cv_rmse, space=voter_space, ens_name='voter',

X_train=X_de_train, y_train=y_de_train,

fixed_params=voter_fixed_params,

pretuned=False, random_state=27, max_evals=50,

trials=ens_ho_results['drop_edit']['voter_tuned']['trials'])

100%|██████████| 50/50 [09:15<00:00, 11.11s/it, best loss: 0.11562031262896297]

100%|██████████| 50/50 [07:55<00:00, 9.51s/it, best loss: 0.11927675656382479]

%%capture

# add and fit fully tuned voting ensembles

ensembles['clean_edit']['voter_tuned'] = \

voter_from_search_params(ens_ho_results['clean_edit']['voter_tuned']['params'],

X_ce_train, y_ce_train, random_state=27)

ensembles['drop_edit']['voter_tuned'] = \

voter_from_search_params(ens_ho_results['drop_edit']['voter_tuned']['params'],

X_de_train, y_de_train, random_state=27)

Stacking

Stacking ensembles fit a meta models to the predictions of base models. To avoid overfitting, one can use folds to generate base models predictions.

We’ll use the implementation mlxtend.StackingCVRegressor. We’ll also choose our meta models from the set of base models (ridge, support vector, and gradient boosted tree regression).

Default base and meta

For a baseline, we’ll consider stack ensembles for which both base and meta models have default parameters. We’ll use all three base models for each, and vary the meta model across the base models.

# add default base and meta without using features in secondary

ensembles = add_stacks(ensembles, model_data, suffix='def',

use_features_in_secondary=False, random_state=27)

# add default base and meta using features in secondary

ensembles = add_stacks(ensembles, model_data, suffix='def',

use_features_in_secondary=True, random_state=27)

Pretuned base and meta

Now we’ll consider stack ensembles for which the base and meta models are already tuned. Again, we’ll use all three base models and vary the meta model across the base models.

# add pretuned base and meta without using features in secondary

ensembles = add_stacks(ensembles, model_data, base_ests=base_pretuned,

meta_ests=base_pretuned, suffix='pretuned',

use_features_in_secondary=False, random_state=27)

# add pretuned base and meta using features in secondary

ensembles = add_stacks(ensembles, model_data, base_ests=base_pretuned,

meta_ests=base_pretuned, suffix='pretuned',

use_features_in_secondary=True, random_state=27)

Fully tuned stacks

Finally, we’ll tune stack ensembles at once, that is we’ll tune both base and meta models simultaneously. As before, we’ll use all three base models and vary the meta model across the base models.

# meta hyperparameter spaces

ridge_meta_space = {'alpha_ridge_meta': hp.loguniform('alpha_ridge_meta', low=-3*np.log(10), high=2*np.log(10))}

svr_meta_space = {'gamma_svr_meta': hp.loguniform('gamma_svr_meta', low=-3*np.log(10), high=2*np.log(10)),

'C_svr_meta': hp.loguniform('C_svr_meta', low=-3*np.log(10), high=2*np.log(10)),

'epsilon_svr_meta': hp.loguniform('epsilon_svr_meta', low=-3*np.log(10), high=2*np.log(10))}

xgb_meta_space = {'max_depth_xgb_meta': ho_scope.int(hp.quniform('max_depth_xgb_meta', low=1, high=3, q=1)),

'n_estimators_xgb_meta': ho_scope.int(hp.quniform('n_estimators_xgb_meta', low=100, high=500, q=50)),

'learning_rate_xgb_meta': hp.loguniform('learning_rate_xgb_meta', low=-4*np.log(10), high=0),

'gamma_xgb_meta': hp.loguniform('gamma_xgb_meta', low=-3*np.log(10), high=2*np.log(10)),

'min_child_weight_xgb_meta': ho_scope.int(hp.quniform('min_child_weight_xgb_meta', low=1, high=7, q=1)),

'subsample_xgb_meta': hp.uniform('subsample_xgb_meta', low=0.25, high=1),

'colsample_bytree_xgb_meta': hp.uniform('colsample_bytree_xgb_meta', low=0.25, high=1),

'colsample_bylevel_xgb_meta': hp.uniform('colsample_bylevel_xgb_meta', low=0.25, high=1),

'colsample_bynode_xgb_meta': hp.uniform('colsample_bynode_xgb_meta', low=0.25, high=1),

'reg_lambda_xgb_meta': hp.loguniform('reg_lambda_xgb_meta', low=-2*np.log(10), high=2*np.log(10)),

'reg_alpha_xgb_meta': hp.loguniform('reg_alpha_xgb_meta', low=-1*np.log(10), high=1*np.log(10)),

}

Ridge regression meta

# ridge meta stack space

ridge_stack_space = {**ridge_meta_space, **base_space}

# store trial objects for restarting training

ens_ho_results['clean_edit']['stack_ridge_tuned'] = {'trials': Trials(), 'params': None}

ens_ho_results['drop_edit']['stack_ridge_tuned'] = {'trials': Trials(), 'params': None}

# tune ridge stack without features in secondary

stack_fixed_params = {'n_jobs': -1, 'use_features_in_secondary': False}

ens_ho_results['clean_edit']['stack_ridge_tuned'] = \

ho_ens_results(obj=ho_ens_cv_rmse, space=ridge_stack_space, ens_name='stack',

X_train=X_ce_train, y_train=y_ce_train, meta_name='ridge',

fixed_params=stack_fixed_params, pretuned=False,

random_state=27, max_evals=50,

trials=ens_ho_results['clean_edit']['stack_ridge_tuned']['trials'])

ens_ho_results['drop_edit']['stack_ridge_tuned'] = \

ho_ens_results(obj=ho_ens_cv_rmse, space=ridge_stack_space, ens_name='stack',

X_train=X_de_train, y_train=y_de_train, meta_name='ridge',

fixed_params=stack_fixed_params, pretuned=False,

random_state=27, max_evals=50,

trials=ens_ho_results['drop_edit']['stack_ridge_tuned']['trials'])

100%|██████████| 50/50 [1:03:53<00:00, 76.67s/it, best loss: 0.11116389697149698]

100%|██████████| 50/50 [1:00:52<00:00, 73.05s/it, best loss: 0.11283371442451827]

%%capture

# add and fit tuned ridge stacks without features in secondary

ensembles['clean_edit']['stack_ridge_tuned'] = \

stack_from_search_params(ens_ho_results['clean_edit']['stack_ridge_tuned']['params'],

X_ce_train, y_ce_train, meta_name='ridge',

random_state=27)

ensembles['drop_edit']['stack_ridge_tuned'] = \

stack_from_search_params(ens_ho_results['drop_edit']['stack_ridge_tuned']['params'],

X_de_train, y_de_train, meta_name='ridge',

random_state=27)

# store trial objects for restarting training

ens_ho_results['clean_edit']['stack_ridge_tuned_second'] = \

{'trials': Trials(), 'params': None}

ens_ho_results['drop_edit']['stack_ridge_tuned_second'] = \

{'trials': Trials(), 'params': None}

# tune ridge stack using features in secondary

stack_fixed_params['use_features_in_secondary'] = True

ens_ho_results['clean_edit']['stack_ridge_tuned_second'] = \

ho_ens_results(obj=ho_ens_cv_rmse, space=ridge_stack_space, ens_name='stack',

X_train=X_ce_train, y_train=y_ce_train, meta_name='ridge',

fixed_params=stack_fixed_params,

pretuned=False, random_state=27, max_evals=50,

trials=ens_ho_results['clean_edit']['stack_ridge_tuned_second']['trials'])

ens_ho_results['drop_edit']['stack_ridge_tuned_second'] = \

ho_ens_results(obj=ho_ens_cv_rmse, space=ridge_stack_space, ens_name='stack',

X_train=X_de_train, y_train=y_de_train, meta_name='ridge',

fixed_params=stack_fixed_params,

pretuned=False, random_state=27, max_evals=50,

trials=ens_ho_results['drop_edit']['stack_ridge_tuned_second']['trials'])

100%|██████████| 50/50 [16:36:46<00:00, 1196.14s/it, best loss: 0.11201848643560201]

100%|██████████| 50/50 [1:09:05<00:00, 82.91s/it, best loss: 0.11459253422339011]

%%capture

# add and fit tuned ridge stacks using features in secondary

ensembles['clean_edit']['stack_ridge_tuned_second'] = \

stack_from_search_params(ens_ho_results['clean_edit']['stack_ridge_tuned_second']['params'],

X_ce_train, y_ce_train, meta_name='ridge',

random_state=27)

ensembles['drop_edit']['stack_ridge_tuned_second'] = \

stack_from_search_params(ens_ho_results['drop_edit']['stack_ridge_tuned_second']['params'],

X_de_train, y_de_train, meta_name='ridge',

random_state=27)

Support Vector Machine meta

# svr meta stack space

svr_stack_space = {**svr_meta_space, **base_space}

# store trial objects for restarting training

ens_ho_results['clean_edit']['stack_svr_tuned'] = {'trials': Trials(), 'params': None}

ens_ho_results['drop_edit']['stack_svr_tuned'] = {'trials': Trials(), 'params': None}

# tune svr stack without features in secondary

stack_fixed_params['use_features_in_secondary'] = False

ens_ho_results['clean_edit']['stack_svr_tuned'] = \

ho_ens_results(obj=ho_ens_cv_rmse, space=svr_stack_space, ens_name='stack',

X_train=X_ce_train, y_train=y_ce_train, meta_name='svr',

fixed_params=stack_fixed_params, pretuned=False,

random_state=27, max_evals=50,

trials=ens_ho_results['clean_edit']['stack_svr_tuned']['trials'])

ens_ho_results['drop_edit']['stack_svr_tuned'] = \

ho_ens_results(obj=ho_ens_cv_rmse, space=svr_stack_space, ens_name='stack',

X_train=X_de_train, y_train=y_de_train, meta_name='svr',

fixed_params=stack_fixed_params, pretuned=False,

random_state=27, max_evals=50,

trials=ens_ho_results['drop_edit']['stack_svr_tuned']['trials'])

100%|██████████| 50/50 [5:52:20<00:00, 422.81s/it, best loss: 0.11151081203889647]

100%|██████████| 50/50 [46:27<00:00, 55.74s/it, best loss: 0.11466092839265946]

# add and fit tuned svr stacks without features in secondary

ensembles['clean_edit']['stack_svr_tuned'] = \

stack_from_search_params(ens_ho_results['clean_edit']['stack_svr_tuned']['params'],

X_ce_train, y_ce_train, meta_name='svr',

random_state=27)

ensembles['drop_edit']['stack_svr_tuned'] = \

stack_from_search_params(ens_ho_results['drop_edit']['stack_svr_tuned']['params'],

X_de_train, y_de_train, meta_name='svr',

random_state=27)

# store trial objects for restarting training

ens_ho_results['clean_edit']['stack_svr_tuned_second'] = \

{'trials': Trials(), 'params': None}

ens_ho_results['drop_edit']['stack_svr_tuned_second'] = \

{'trials': Trials(), 'params': None}

# tune svr stack using features in secondary

stack_fixed_params['use_features_in_secondary'] = True

ens_ho_results['clean_edit']['stack_svr_tuned_second'] = \

ho_ens_results(obj=ho_ens_cv_rmse, space=svr_stack_space, ens_name='stack',

X_train=X_ce_train, y_train=y_ce_train, meta_name='svr',

fixed_params=stack_fixed_params, pretuned=False,

random_state=27, max_evals=50,

trials=ens_ho_results['clean_edit']['stack_svr_tuned_second']['trials'])

ens_ho_results['drop_edit']['stack_svr_tuned_second'] = \

ho_ens_results(obj=ho_ens_cv_rmse, space=svr_stack_space, ens_name='stack',

X_train=X_de_train, y_train=y_de_train, meta_name='svr',

fixed_params=stack_fixed_params, pretuned=False,

random_state=27, max_evals=50,

trials=ens_ho_results['drop_edit']['stack_svr_tuned_second']['trials'])

# add and fit tuned svr stacks using features in secondary

ensembles['clean_edit']['stack_svr_tuned_second'] = \

stack_from_search_params(ens_ho_results['clean_edit']['stack_svr_tuned_second']['params'],

X_ce_train, y_ce_train, meta_name='ridge',

random_state=27)

ensembles['drop_edit']['stack_svr_tuned_second'] = \

stack_from_search_params(ens_ho_results['drop_edit']['stack_svr_tuned_second']['params'],

X_de_train, y_de_train, meta_name='ridge',

random_state=27)

Gradient Boosted Tree meta

# xgb meta stack space

xgb_stack_space = {**xgb_meta_space, **base_space}

# store trial objects for restarting training

ens_ho_results['clean_edit']['stack_xgb_tuned'] = {'trials': Trials(), 'params': None}

ens_ho_results['drop_edit']['stack_xgb_tuned'] = {'trials': Trials(), 'params': None}

# tune xgb stack without features in secondary

stack_fixed_params['use_features_in_secondary'] = False

ens_ho_results['clean_edit']['stack_xgb_tuned'] = \

ho_ens_results(obj=ho_ens_cv_rmse, space=xgb_stack_space, ens_name='stack',

X_train=X_ce_train, y_train=y_ce_train, meta_name='xgb',

fixed_params=stack_fixed_params, pretuned=False,

random_state=27, max_evals=50,

trials=ens_ho_results['clean_edit']['stack_xgb_tuned']['trials'])

ens_ho_results['drop_edit']['stack_xgb_tuned'] = \

ho_ens_results(obj=ho_ens_cv_rmse, space=xgb_stack_space, ens_name='stack',

X_train=X_de_train, y_train=y_de_train, meta_name='xgb',

fixed_params=stack_fixed_params, pretuned=False,

random_state=27, max_evals=50,

trials=ens_ho_results['drop_edit']['stack_xgb_tuned']['trials'])

# add and fit tuned xgb stacks without features in secondary

ensembles['clean_edit']['stack_xgb_tuned'] = \

stack_from_search_params(ens_ho_results['clean_edit']['stack_xgb_tuned']['params'],

X_ce_train, y_ce_train, meta_name='xgb',

random_state=27)

ensembles['drop_edit']['stack_xgb_tuned'] = \

stack_from_search_params(ens_ho_results['drop_edit']['stack_xgb_tuned']['params'],

X_de_train, y_de_train, meta_name='xgb',

random_state=27)

# store trial objects for restarting training

ens_ho_results['clean_edit']['stack_xgb_tuned_second'] = \

{'trials': Trials(), 'params': None}

ens_ho_results['drop_edit']['stack_xgb_tuned_second'] = \

{'trials': Trials(), 'params': None}

# tune xgb stack with features in secondary

stack_fixed_params['use_features_in_secondary'] = True

ens_ho_results['clean_edit']['stack_xgb_tuned_second'] = \

ho_ens_results(obj=ho_ens_cv_rmse, space=xgb_stack_space, ens_name='stack',

X_train=X_ce_train, y_train=y_ce_train, meta_name='xgb',

fixed_params=stack_fixed_params, pretuned=False,

random_state=27, max_evals=50,

trials=ens_ho_results['clean_edit']['stack_xgb_tuned_second']['trials'])

ens_ho_results['drop_edit']['stack_xgb_tuned_second'] = \

ho_ens_results(obj=ho_ens_cv_rmse, space=xgb_stack_space, ens_name='stack',

X_train=X_de_train, y_train=y_de_train, meta_name='xgb',

fixed_params=stack_fixed_params, pretuned=False,

random_state=27, max_evals=50,

trials=ens_ho_results['drop_edit']['stack_xgb_tuned_second']['trials'])

# add and fit tuned xgb stacks with features in secondary

ensembles['clean_edit']['stack_xgb_tuned_second'] = \

stack_from_search_params(ens_ho_results['clean_edit']['stack_xgb_tuned_second']['params'],

X_ce_train, y_ce_train, meta_name='xgb', random_state=27)

ensembles['drop_edit']['stack_xgb_tuned_second'] = \

stack_from_search_params(ens_ho_results['drop_edit']['stack_xgb_tuned_second']['params'],

X_de_train, y_de_train, meta_name='xgb', random_state=27)

Compare ensembles

Now we look at the performance of all our ensemble models.

# compare results of tuned models -- warning this takes a LONG time

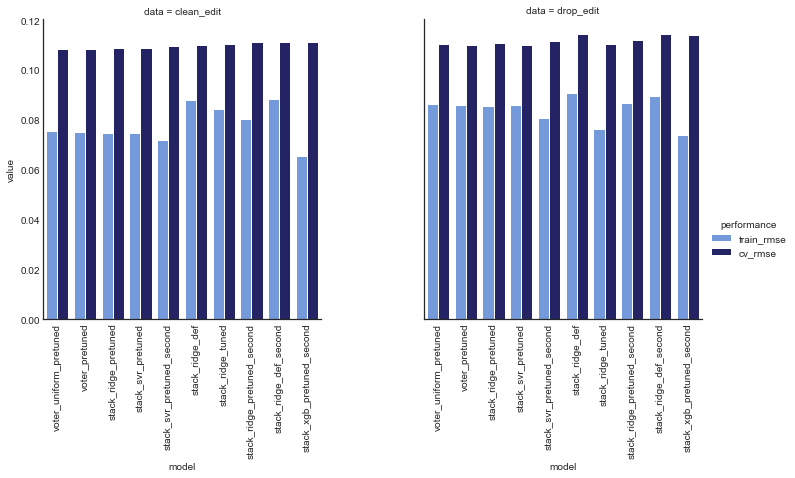

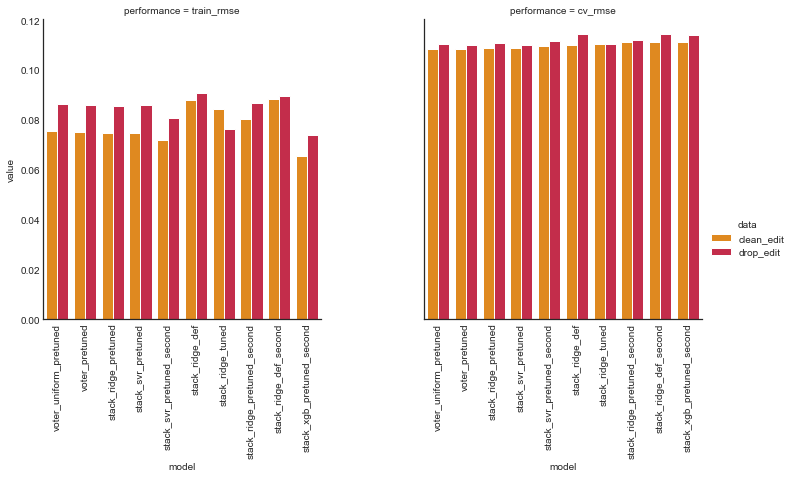

ens_comp_df = compare_performance(ensembles, model_data, random_state=27)

ens_comp_df = ens_comp_df.reset_index(drop=True)

# comparison of ensembles sorted by cv rmse on clean edit dataset

ens_comp_df.sort_values(by=('clean_edit', 'cv_rmse'), ascending=True)

| data | model | clean_edit | drop_edit | ||

|---|---|---|---|---|---|

| performance | train_rmse | cv_rmse | train_rmse | cv_rmse | |

| 0 | voter_uniform_pretuned | 0.075474 | 0.108401 | 0.0865722 | 0.110661 |

| 1 | voter_pretuned | 0.075299 | 0.1086 | 0.0861689 | 0.110256 |

| 2 | stack_ridge_pretuned | 0.0746405 | 0.1087 | 0.0854078 | 0.110722 |

| 3 | stack_svr_pretuned | 0.0748075 | 0.108715 | 0.0861604 | 0.110122 |

| 4 | stack_svr_pretuned_second | 0.0720033 | 0.109798 | 0.0806914 | 0.111473 |

| 5 | stack_ridge_def | 0.0878178 | 0.109917 | 0.0909945 | 0.114609 |

| 6 | stack_ridge_tuned | 0.084249 | 0.110514 | 0.0762328 | 0.110347 |

| 7 | stack_ridge_pretuned_second | 0.0803682 | 0.111236 | 0.0867375 | 0.112014 |

| 8 | stack_ridge_def_second | 0.0882177 | 0.111284 | 0.0896656 | 0.114543 |

| 9 | stack_xgb_pretuned_second | 0.065358 | 0.111331 | 0.0737561 | 0.113974 |

| 10 | stack_svr_def | 0.0902256 | 0.112275 | 0.093318 | 0.115215 |

| 11 | voter_def | 0.092585 | 0.112753 | 0.0961106 | 0.116457 |

| 12 | stack_svr_tuned | 0.0946273 | 0.112926 | 0.0943019 | 0.114366 |

| 13 | stack_xgb_pretuned | 0.081221 | 0.112994 | 0.0917646 | 0.116637 |

| 14 | stack_xgb_def_second | 0.0787932 | 0.11329 | 0.0787003 | 0.11728 |

| 15 | voter_tuned | 0.0706802 | 0.114352 | 0.106915 | 0.120561 |

| 16 | stack_xgb_def | 0.0910824 | 0.114399 | 0.094562 | 0.119964 |

| 17 | stack_ridge_tuned_second | 0.0831083 | 0.116366 | 0.0842815 | 0.120442 |

| 18 | stack_svr_def_second | 0.0976675 | 0.11676 | 0.0987419 | 0.120366 |

# comparison of ensembles sorted by cv rmse on drop edit dataset

ens_comp_df.sort_values(by=('drop_edit', 'cv_rmse'), ascending=True)

| data | model | clean_edit | drop_edit | ||

|---|---|---|---|---|---|

| performance | train_rmse | cv_rmse | train_rmse | cv_rmse | |

| 3 | stack_svr_pretuned | 0.0748075 | 0.108715 | 0.0861604 | 0.110122 |

| 1 | voter_pretuned | 0.075299 | 0.1086 | 0.0861689 | 0.110256 |

| 6 | stack_ridge_tuned | 0.084249 | 0.110514 | 0.0762328 | 0.110347 |

| 0 | voter_uniform_pretuned | 0.075474 | 0.108401 | 0.0865722 | 0.110661 |

| 2 | stack_ridge_pretuned | 0.0746405 | 0.1087 | 0.0854078 | 0.110722 |

| 4 | stack_svr_pretuned_second | 0.0720033 | 0.109798 | 0.0806914 | 0.111473 |

| 7 | stack_ridge_pretuned_second | 0.0803682 | 0.111236 | 0.0867375 | 0.112014 |

| 9 | stack_xgb_pretuned_second | 0.065358 | 0.111331 | 0.0737561 | 0.113974 |

| 12 | stack_svr_tuned | 0.0946273 | 0.112926 | 0.0943019 | 0.114366 |

| 8 | stack_ridge_def_second | 0.0882177 | 0.111284 | 0.0896656 | 0.114543 |

| 5 | stack_ridge_def | 0.0878178 | 0.109917 | 0.0909945 | 0.114609 |

| 10 | stack_svr_def | 0.0902256 | 0.112275 | 0.093318 | 0.115215 |

| 11 | voter_def | 0.092585 | 0.112753 | 0.0961106 | 0.116457 |

| 13 | stack_xgb_pretuned | 0.081221 | 0.112994 | 0.0917646 | 0.116637 |