islr notes and exercises from An Introduction to Statistical Learning

4. Logistic Regression

Exercise 10: Classifying Direction in the Weekly dataset

- Preparing the Data

- a. Numerical and graphical summaries

- b. Logistic Regression Classification of

DirectionusingLagandVolumepredictors - c. Confusion Matrix

- d. Logistic Regression Classification of

DirectionusingLag2predictor - e. Other classification models of

DirectionusingLag2predictor - h. Which method has the best results?

- i. Feature and Model Selection

- Get all predictor interactions

- Choose some transformations

- Random data tweak

- Comparison of Logit, LDA, QDA, and KNN models on a single random data tweak

- <a href="#comparison-of-logit-lda-qda-and-knn-models-over--data-tweaks" data-toc-modified-id="Comparison-of-Logit,-LDA,-QDA,-and-KNN-models-over--data-tweaks-8.5">Comparison of Logit, LDA, QDA, and KNN models over data tweaks</a>

- Analysis of Comparisons

Preparing the Data

Import

import pandas as pd

weekly = pd.read_csv('../../datasets/Weekly.csv', index_col=0)

weekly.head()

| Year | Lag1 | Lag2 | Lag3 | Lag4 | Lag5 | Volume | Today | Direction | |

|---|---|---|---|---|---|---|---|---|---|

| 1 | 1990 | 0.816 | 1.572 | -3.936 | -0.229 | -3.484 | 0.154976 | -0.270 | Down |

| 2 | 1990 | -0.270 | 0.816 | 1.572 | -3.936 | -0.229 | 0.148574 | -2.576 | Down |

| 3 | 1990 | -2.576 | -0.270 | 0.816 | 1.572 | -3.936 | 0.159837 | 3.514 | Up |

| 4 | 1990 | 3.514 | -2.576 | -0.270 | 0.816 | 1.572 | 0.161630 | 0.712 | Up |

| 5 | 1990 | 0.712 | 3.514 | -2.576 | -0.270 | 0.816 | 0.153728 | 1.178 | Up |

weekly.info()

<class 'pandas.core.frame.DataFrame'>

Int64Index: 1089 entries, 1 to 1089

Data columns (total 9 columns):

Year 1089 non-null int64

Lag1 1089 non-null float64

Lag2 1089 non-null float64

Lag3 1089 non-null float64

Lag4 1089 non-null float64

Lag5 1089 non-null float64

Volume 1089 non-null float64

Today 1089 non-null float64

Direction 1089 non-null object

dtypes: float64(7), int64(1), object(1)

memory usage: 85.1+ KB

Preprocessing

Converting qualitative variables to quantitative

Don’t see any null values but let’s check

weekly.isna().sum().sum()

0

Direction is a qualitative variable encoded as a string; let’s encode it numerically

import sklearn.preprocessing as skl_preprocessing

# create and fit label encoder

direction_le = skl_preprocessing.LabelEncoder()

direction_le.fit(weekly.Direction)

# replace string encoding with numeric

weekly['Direction_num'] = direction_le.transform(weekly.Direction)

weekly.Direction_num.head()

1 0

2 0

3 1

4 1

5 1

Name: Direction_num, dtype: int64

direction_le.classes_

array(['Down', 'Up'], dtype=object)

direction_le.transform(direction_le.classes_)

array([0, 1])

So the encoding is {Down:0, Up:1}

a. Numerical and graphical summaries

Here’s a description of the dataset from the R documentation

Weekly S&P Stock Market Data

Description

Weekly percentage returns for the S&P 500 stock index between 1990 and 2010.

Usage

Weekly

Format

A data frame with 1089 observations on the following 9 variables.

Year

The year that the observation was recorded

Lag1

Percentage return for previous week

Lag2

Percentage return for 2 weeks previous

Lag3

Percentage return for 3 weeks previous

Lag4

Percentage return for 4 weeks previous

Lag5

Percentage return for 5 weeks previous

Volume

Volume of shares traded (average number of daily shares traded in billions)

Today

Percentage return for this week

Direction

A factor with levels Down and Up indicating whether the market had a positive or negative return on a given week

Source

Raw values of the S&P 500 were obtained from Yahoo Finance and then converted to percentages and lagged.

Let’s look at summary statistics

weekly.describe()

| Year | Lag1 | Lag2 | Lag3 | Lag4 | Lag5 | Volume | Today | Direction_num | |

|---|---|---|---|---|---|---|---|---|---|

| count | 1089.000000 | 1089.000000 | 1089.000000 | 1089.000000 | 1089.000000 | 1089.000000 | 1089.000000 | 1089.000000 | 1089.000000 |

| mean | 2000.048669 | 0.150585 | 0.151079 | 0.147205 | 0.145818 | 0.139893 | 1.574618 | 0.149899 | 0.555556 |

| std | 6.033182 | 2.357013 | 2.357254 | 2.360502 | 2.360279 | 2.361285 | 1.686636 | 2.356927 | 0.497132 |

| min | 1990.000000 | -18.195000 | -18.195000 | -18.195000 | -18.195000 | -18.195000 | 0.087465 | -18.195000 | 0.000000 |

| 25% | 1995.000000 | -1.154000 | -1.154000 | -1.158000 | -1.158000 | -1.166000 | 0.332022 | -1.154000 | 0.000000 |

| 50% | 2000.000000 | 0.241000 | 0.241000 | 0.241000 | 0.238000 | 0.234000 | 1.002680 | 0.241000 | 1.000000 |

| 75% | 2005.000000 | 1.405000 | 1.409000 | 1.409000 | 1.409000 | 1.405000 | 2.053727 | 1.405000 | 1.000000 |

| max | 2010.000000 | 12.026000 | 12.026000 | 12.026000 | 12.026000 | 12.026000 | 9.328214 | 12.026000 | 1.000000 |

-

All the variables ranges look good (e.g. no negative values for volume)

-

The

Lagvariables andTodayall have very similar summary statistics, as expected. -

Of particular interest is

Direction_num, which has a mean of and a standard deviation of ! That’s what we’ll be trying to predict later in the exercise, which will be interesting.

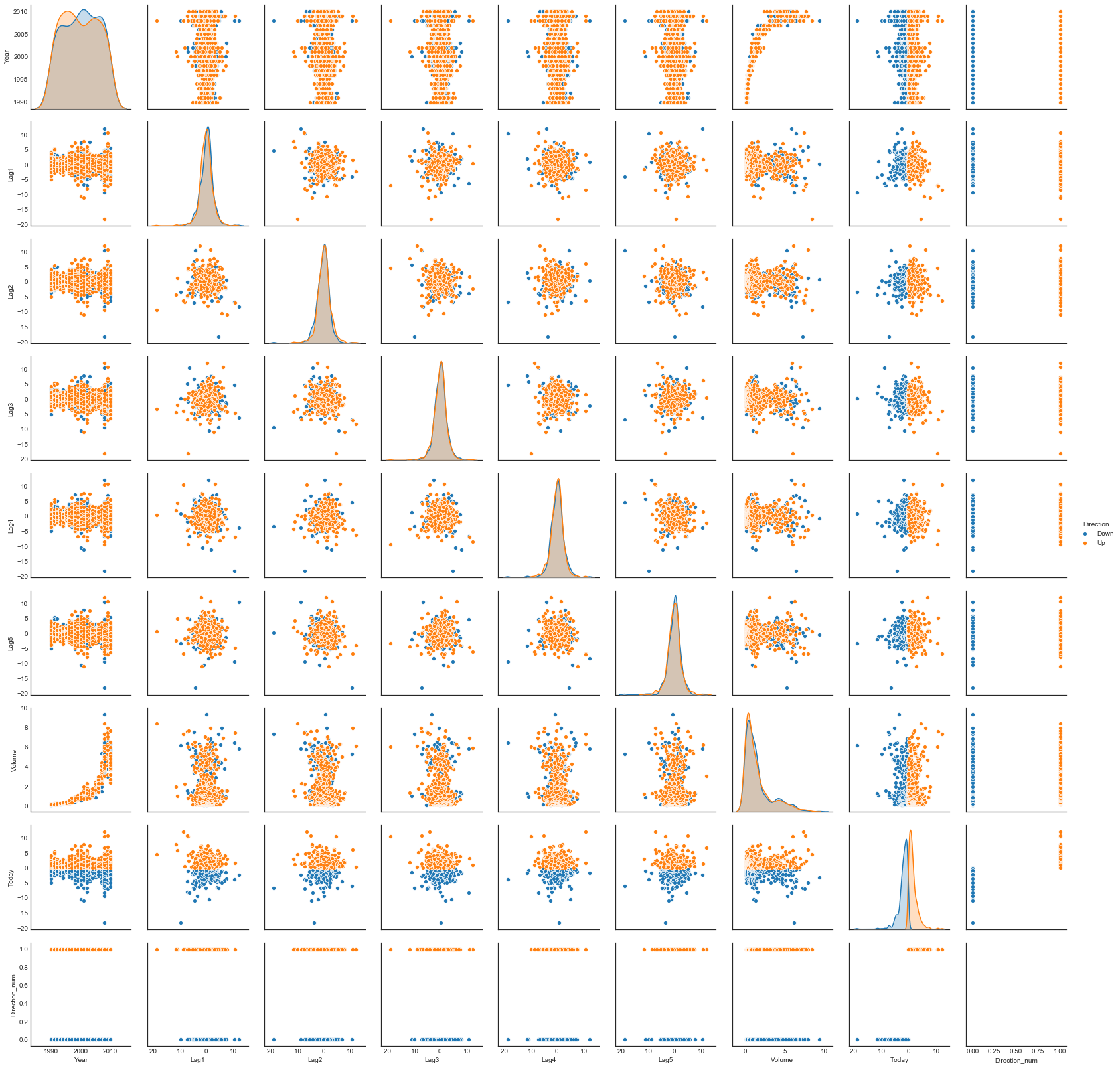

Let’s look at distributions

import seaborn as sns

import matplotlib.pyplot as plt

%matplotlib inline

plt.style.use('seaborn-white')

sns.set_style('white')

import warnings

warnings.filterwarnings('ignore')

import numpy as np

sns.pairplot(weekly, hue='Direction')

<seaborn.axisgrid.PairGrid at 0x1a2515d208>

The return variables are concentrated

The return variables (i.e. Lag and Today variables) are “tight” instead of spread out, i.e. fairly concentrated about their mean.

Here are the deviations of all variables as percentages of the magnitude of their ranges

weekly_num = weekly.drop('Direction', axis=1)

round(100 * (weekly_num.std() / (weekly_num.max() - weekly_num.min())), 2)

Year 30.17

Lag1 7.80

Lag2 7.80

Lag3 7.81

Lag4 7.81

Lag5 7.81

Volume 18.25

Today 7.80

Direction_num 49.71

dtype: float64

Return variables are nearly uncorrelated

In the pairplot there is a visible lack of pairwise sample correlation among the return variables.

weekly.corr()

| Year | Lag1 | Lag2 | Lag3 | Lag4 | Lag5 | Volume | Today | Direction_num | |

|---|---|---|---|---|---|---|---|---|---|

| Year | 1.000000 | -0.032289 | -0.033390 | -0.030006 | -0.031128 | -0.030519 | 0.841942 | -0.032460 | -0.022200 |

| Lag1 | -0.032289 | 1.000000 | -0.074853 | 0.058636 | -0.071274 | -0.008183 | -0.064951 | -0.075032 | -0.050004 |

| Lag2 | -0.033390 | -0.074853 | 1.000000 | -0.075721 | 0.058382 | -0.072499 | -0.085513 | 0.059167 | 0.072696 |

| Lag3 | -0.030006 | 0.058636 | -0.075721 | 1.000000 | -0.075396 | 0.060657 | -0.069288 | -0.071244 | -0.022913 |

| Lag4 | -0.031128 | -0.071274 | 0.058382 | -0.075396 | 1.000000 | -0.075675 | -0.061075 | -0.007826 | -0.020549 |

| Lag5 | -0.030519 | -0.008183 | -0.072499 | 0.060657 | -0.075675 | 1.000000 | -0.058517 | 0.011013 | -0.018168 |

| Volume | 0.841942 | -0.064951 | -0.085513 | -0.069288 | -0.061075 | -0.058517 | 1.000000 | -0.033078 | -0.017995 |

| Today | -0.032460 | -0.075032 | 0.059167 | -0.071244 | -0.007826 | 0.011013 | -0.033078 | 1.000000 | 0.720025 |

| Direction_num | -0.022200 | -0.050004 | 0.072696 | -0.022913 | -0.020549 | -0.018168 | -0.017995 | 0.720025 | 1.000000 |

Indeed the magnitudes of the sample correlations for these pairs are quite small.

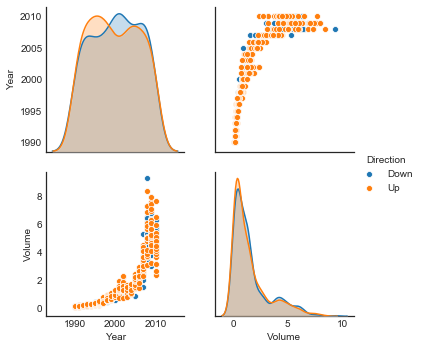

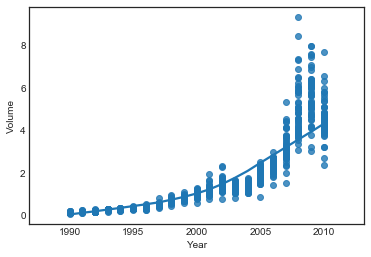

Volume correlates with Year

sns.pairplot(weekly, vars=['Year', 'Volume'], hue='Direction')

<seaborn.axisgrid.PairGrid at 0x1a28503780>

sns.regplot(weekly.Year, weekly.Volume, lowess=True)

<matplotlib.axes._subplots.AxesSubplot at 0x1a2a543be0>

b. Logistic Regression Classification of Direction using Lag and Volume predictors

import statsmodels.api as sm

# predictor labels

predictors = ['Lag' + stri. for i in range(1, 6)]

predictors += ['Volume']

# fit and summarize model

sm_logit_model_full = sm.Logit(weekly.Direction_num, sm.add_constant(weekly[predictors]))

sm_logit_model_full.fit().summary()

Optimization terminated successfully.

Current function value: 0.682441

Iterations 4

| Dep. Variable: | Direction_num | No. Observations: | 1089 |

|---|---|---|---|

| Model: | Logit | Df Residuals: | 1082 |

| Method: | MLE | Df Model: | 6 |

| Date: | Mon, 26 Nov 2018 | Pseudo R-squ.: | 0.006580 |

| Time: | 17:27:33 | Log-Likelihood: | -743.18 |

| converged: | True | LL-Null: | -748.10 |

| LLR p-value: | 0.1313 |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | 0.2669 | 0.086 | 3.106 | 0.002 | 0.098 | 0.435 |

| Lag1 | -0.0413 | 0.026 | -1.563 | 0.118 | -0.093 | 0.010 |

| Lag2 | 0.0584 | 0.027 | 2.175 | 0.030 | 0.006 | 0.111 |

| Lag3 | -0.0161 | 0.027 | -0.602 | 0.547 | -0.068 | 0.036 |

| Lag4 | -0.0278 | 0.026 | -1.050 | 0.294 | -0.080 | 0.024 |

| Lag5 | -0.0145 | 0.026 | -0.549 | 0.583 | -0.066 | 0.037 |

| Volume | -0.0227 | 0.037 | -0.616 | 0.538 | -0.095 | 0.050 |

Only the intercept and Lag2 and appear to be statistically significant

c. Confusion Matrix

import sklearn.linear_model as skl_linear_model

# fit model

skl_logit_model_full = skl_linear_model.LogisticRegression()

X, Y = sm.add_constant(weekly[predictors]).values, weekly.Direction_num.values

skl_logit_model_full.fit(X, Y)

LogisticRegression(C=1.0, class_weight=None, dual=False, fit_intercept=True,

intercept_scaling=1, max_iter=100, multi_class='warn',

n_jobs=None, penalty='l2', random_state=None, solver='warn',

tol=0.0001, verbose=0, warm_start=False)

# check paramaters are close in the two models

abs(skl_logit_model_full.coef_ - sm_logit_model_full.fit().params.values)

Optimization terminated successfully.

Current function value: 0.682441

Iterations 4

array([[1.33953314e-01, 6.15092984e-05, 3.94405141e-06, 4.06643634e-05,

5.96004698e-05, 3.92562567e-05, 3.22507048e-04]])

import sklearn.metrics as skl_metrics

# confusion matrix

confusion_array = skl_metrics.confusion_matrix(Y, skl_logit_model_full.predict(X))

confusion_array

array([[ 54, 430],

[ 47, 558]])

# confusion data frame

col_index = pd.MultiIndex.from_product([['Pred'], [0, 1]])

row_index = pd.MultiIndex.from_product([['Actual'], [0, 1]])

confusion_df = pd.DataFrame(confusion_array, columns=col_index, index=row_index)

confusion_df.loc[: ,('Pred','Total')] = confusion_df.Pred[0] + confusion_df.Pred[1]

confusion_df.loc[('Actual','Total'), :] = (confusion_df.loc[('Actual',0), :] +

confusion_df.loc[('Actual',1), :])

confusion_df.astype('int32')

| Pred | ||||

|---|---|---|---|---|

| 0 | 1 | Total | ||

| Actual | 0 | 54 | 430 | 484 |

| 1 | 47 | 558 | 605 | |

| Total | 101 | 988 | 1089 | |

Performance rates of interest from the confusion matrix

Recall that for a binary classifier the confusion matrix shows

where

Also recall the following rates of interest

- The accuracy of the classifier is the proportion of correctly classified observations

i.e., “How often is the model right?”

- The misclassification rate (or error rate) is the proportion of incorrectly classified observations

i.e., “How often is the model wrong?”

- The null error rate is the proportion of the majority class

i.e. “How often would we be wrong if we always predicted the majority class”

- The true positive rate (or sensitivity or recall) is the ratio of true positives to actual positives

, “How often is the model right for actual positives ()?”

- The false positive rate is the ratio of false positives to actual negatives

i.e., “How often is the model wrong for actual positives?”

- The true negative rate or specificity is the ratio of true negatives to actual negatives

i.e., “How often is the model right for actual negatives ()?”

- The false negative rate is the ratio of true negatives to actual negatives

i.e., “How often is the model wrong for actual negatives ()?”

- The precision is the ratio of true positives to predicted positives

i.e., “How often are the models’ positive predictions right?”

- The prevalence is the ratio of actual positives to total observations

i.e., “How often do actual positives occur in the sample?”

Analyzing model performance rates

# necessary variables

n = confusion_df.loc[('Actual', 'Total'), ('Pred', 'Total')]

TN = confusion_df.loc[('Actual', 0), ('Pred', 0)]

FP = confusion_df.loc[('Actual', 0), ('Pred', 1)]

FN = confusion_df.loc[('Actual', 1), ('Pred', 0)]

TP = confusion_df.loc[('Actual', 1), ('Pred', 1)]

# compute rates

rates = {}

rates['accuracy'] = (TP + TN) / n

rates['error rate'] = (FP + FN) / n

rates['null error'] = max(FN + TP, FP + TN) / n

rates['TP rate'] = TP / (FN + TP)

rates['FP rate'] = FP / (FN + TP)

rates['TN rate'] = TN / (FP + TN)

rates['FN rate'] = FN / (FP + TN)

rates['precision'] = TP / (FP + TP)

rates['prevalence'] = (FN + TP) / n

# store results

model_perf_rates_df = pd.DataFrame(rates, index=[0])

model_perf_rates_df

| accuracy | error rate | null error | TP rate | FP rate | TN rate | FN rate | precision | prevalence | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.561983 | 0.438017 | 0.555556 | 0.922314 | 0.710744 | 0.11157 | 0.097107 | 0.564777 | 0.555556 |

Observations

-

The accuracy is so the model is right a bit more than half the time

-

The error rate is so the model is wrong a bit less than half the time

-

The “null error rate” is the error rate of the “null classifier” which always predicts the majority class, which in this case is . Thus our model is about as accurate as the null classifier.

-

The true positive and false positive rates are relatively high. The true negative and false negative rates are relatively low. This makes sense – inspection of the confusion matrix shows that the model predicts positives almost an order of magnitude more often

-

The precision is so the model correctly predicts positives a little more than half the time

-

The prevalence is also so positives occur in the sample a little more than half the time

We’ll package this functionality for later use:

def confusion_results(X, y, skl_model_fit):

# get confusion array

confusion_array = skl_metrics.confusion_matrix(y, skl_model_fit.predict(X))

# necessary variables

n = np.sum(confusion_array)

TN = confusion_array[0, 0]

FP = confusion_array[0, 1]

FN = confusion_array[1, 0]

TP = confusion_array[1, 1]

# compute rates

rates = {}

rates['accuracy'] = (TP + TN) / n

rates['error rate'] = (FP + FN) / n

rates['null error'] = max(FN + TP, FP + TN) / n

rates['TP rate'] = TP / (FN + TP)

rates['FP rate'] = FP / (FN + TP)

rates['TN rate'] = TN / (FP + TN)

rates['FN rate'] = FN / (FP + TN)

rates['precision'] = TP / (FP + TP)

rates['prevalence'] = (FN + TP) / n

# return results

return pd.DataFrame(rates, index=[0])

confusion_results(X, Y, skl_logit_model_full.fit(X, Y))

| accuracy | error rate | null error | TP rate | FP rate | TN rate | FN rate | precision | prevalence | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.561983 | 0.438017 | 0.555556 | 0.922314 | 0.710744 | 0.11157 | 0.097107 | 0.564777 | 0.555556 |

d. Logistic Regression Classification of Direction using Lag2 predictor

In this section we do some feature selection. Since in b. we found that only Lag2 was a significant feature, we’ll eliminate the others. Further, we’ll train on the years 1990 to 2008 and test on 2009 to 2010

# train/test split

weekly_test, weekly_train = weekly[weekly['Year'] <= 2008], weekly[weekly['Year'] > 2008]

X_train, y_train = sm.add_constant(weekly_train['Lag2']), weekly_train['Direction_num']

X_test, y_test = sm.add_constant(weekly_test['Lag2']), weekly_test['Direction_num']

# fit new model

skl_logit_model_lag2 = skl_linear_model.LogisticRegression()

# confusion matrix

confusion_results(X_test, y_test, skl_logit_model_lag2.fit(X_train, y_train))

| accuracy | error rate | null error | TP rate | FP rate | TN rate | FN rate | precision | prevalence | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.550254 | 0.449746 | 0.552284 | 0.963235 | 0.777574 | 0.040816 | 0.045351 | 0.553326 | 0.552284 |

The accuracy is actually slightly worse than the full model

e. Other classification models of Direction using Lag2 predictor

LDA

import sklearn.discriminant_analysis as skl_discriminant_analysis

skl_LDA_model_lag2 = skl_discriminant_analysis.LinearDiscriminantAnalysis()

# confusion matrix

confusion_results(X_test, y_test, skl_LDA_model_lag2.fit(X_train, y_train))

| accuracy | error rate | null error | TP rate | FP rate | TN rate | FN rate | precision | prevalence | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.550254 | 0.449746 | 0.552284 | 0.965074 | 0.779412 | 0.038549 | 0.043084 | 0.553214 | 0.552284 |

# accuracy

skl_metrics.accuracy_score(y_test, skl_LDA_model_lag2.predict(X_test))

0.550253807106599

Nearly identical to skl_logit_model_lag2!

QDA

skl_QDA_model_lag2 = skl_discriminant_analysis.QuadraticDiscriminantAnalysis()

# confusion matrix

confusion_results(X_test, y_test, skl_QDA_model_lag2.fit(X_train, y_train))

| accuracy | error rate | null error | TP rate | FP rate | TN rate | FN rate | precision | prevalence | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.447716 | 0.552284 | 0.552284 | 0.0 | 0.0 | 1.0 | 1.23356 | NaN | 0.552284 |

Worse accuracy than Logistic Regression and LDA

KNN

import sklearn.neighbors as skl_neighbors

skl_KNN_model_lag2 = skl_neighbors.KNeighborsClassifier(n_neighbors=1)

# confusion matrix

confusion_results(X_test, y_test, skl_KNN_model_lag2.fit(X_train, y_train))

| accuracy | error rate | null error | TP rate | FP rate | TN rate | FN rate | precision | prevalence | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.518782 | 0.481218 | 0.552284 | 0.626838 | 0.498162 | 0.385488 | 0.460317 | 0.55719 | 0.552284 |

Comparing results

For neatness and ease of comparison, we’ll package all these results

def confusion_comparison(X, y, models):

df = pd.concat([confusion_results(X, y, models[model_name])

for model_name in models])

df['Model'] = list(models.keys())

return df.set_index('Model')

models = {'Logit': skl_logit_model_lag2, 'LDA': skl_LDA_model_lag2,

'QDA': skl_QDA_model_lag2, 'KNN': skl_KNN_model_lag2}

for model_name in models:

models[model_name] = models[model_name].fit(X_train, y_train)

conf_comp_df = confusion_comparison(X_test, y_test, models)

conf_comp_df

| accuracy | error rate | null error | TP rate | FP rate | TN rate | FN rate | precision | prevalence | |

|---|---|---|---|---|---|---|---|---|---|

| Model | |||||||||

| Logit | 0.550254 | 0.449746 | 0.552284 | 0.963235 | 0.777574 | 0.040816 | 0.045351 | 0.553326 | 0.552284 |

| LDA | 0.550254 | 0.449746 | 0.552284 | 0.965074 | 0.779412 | 0.038549 | 0.043084 | 0.553214 | 0.552284 |

| QDA | 0.447716 | 0.552284 | 0.552284 | 0.000000 | 0.000000 | 1.000000 | 1.233560 | NaN | 0.552284 |

| KNN | 0.518782 | 0.481218 | 0.552284 | 0.626838 | 0.498162 | 0.385488 | 0.460317 | 0.557190 | 0.552284 |

h. Which method has the best results?

As measured by accuracy, Logit and LDA models are tied, with KNN not too far behind and QDA a more distant third.

With respect to other confusion metrics, Logit and LDA are nearly identical

i. Feature and Model Selection

In this section, we’ll experiment to try to find improved performance on the test data. We’ll try:

- Different subsets of the predictors

- Interactions among the predictors

- Transformations of the predictors

- Different values of for KNN

Get all predictor interactions

from itertools import combinations

# all pairs of columns in weekly except year and direction

df = weekly.drop(['Year', 'Direction', 'Direction_num'], axis=1)

col_pairs = combinations(df.columns, 2)

# assemble interactions in dataframe

interaction_df = pd.DataFrame({col1 + ':' + col2: weekly[col1]*weekly[col2]

for (col1, col2) in col_pairs})

# concat data frames

dir_df = weekly[['Direction', 'Direction_num']]

weekly_interact = pd.concat([weekly.drop(['Direction', 'Direction_num'], axis=1),

interaction_df, dir_df], axis=1)

weekly_interact.head()

| Year | Lag1 | Lag2 | Lag3 | Lag4 | Lag5 | Volume | Today | Lag1:Lag2 | Lag1:Lag3 | ... | Lag3:Volume | Lag3:Today | Lag4:Lag5 | Lag4:Volume | Lag4:Today | Lag5:Volume | Lag5:Today | Volume:Today | Direction | Direction_num | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 1990 | 0.816 | 1.572 | -3.936 | -0.229 | -3.484 | 0.154976 | -0.270 | 1.282752 | -3.211776 | ... | -0.609986 | 1.062720 | 0.797836 | -0.035490 | 0.061830 | -0.539936 | 0.940680 | -0.041844 | Down | 0 |

| 2 | 1990 | -0.270 | 0.816 | 1.572 | -3.936 | -0.229 | 0.148574 | -2.576 | -0.220320 | -0.424440 | ... | 0.233558 | -4.049472 | 0.901344 | -0.584787 | 10.139136 | -0.034023 | 0.589904 | -0.382727 | Down | 0 |

| 3 | 1990 | -2.576 | -0.270 | 0.816 | 1.572 | -3.936 | 0.159837 | 3.514 | 0.695520 | -2.102016 | ... | 0.130427 | 2.867424 | -6.187392 | 0.251265 | 5.524008 | -0.629120 | -13.831104 | 0.561669 | Up | 1 |

| 4 | 1990 | 3.514 | -2.576 | -0.270 | 0.816 | 1.572 | 0.161630 | 0.712 | -9.052064 | -0.948780 | ... | -0.043640 | -0.192240 | 1.282752 | 0.131890 | 0.580992 | 0.254082 | 1.119264 | 0.115081 | Up | 1 |

| 5 | 1990 | 0.712 | 3.514 | -2.576 | -0.270 | 0.816 | 0.153728 | 1.178 | 2.501968 | -1.834112 | ... | -0.396003 | -3.034528 | -0.220320 | -0.041507 | -0.318060 | 0.125442 | 0.961248 | 0.181092 | Up | 1 |

5 rows × 31 columns

Choose some transformations

# list of transformations

from numpy import sqrt, sin, log, exp, power

# power functions with odd exponent to preserve sign of inputs

def power_3(array):

return np.power(array, 3)

def power_5(array):

return np.power(array, 3)

def power_7(array):

return np.power(array, 4)

# transformations are functions with domain all real numbers

transforms = [power_3, power_5, power_7, sin, exp]

transforms

[<function __main__.power_3(array)>,

<function __main__.power_5(array)>,

<function __main__.power_7(array)>,

<ufunc 'sin'>,

<ufunc 'exp'>]

Random data tweak

We’ll write a simple function which returns a dataset which has

- as predictors a random subset of the predictors and interactions of the original dataset (i.e. a random subset of the columns of

weekly_interact) - a random subset of its predictors transformed by a random choice of transformations from

transform

We call such a dataset a “random data tweak”

import numpy as np

def random_data_tweak(weekly_interact, transforms):

# drop undersirable columns

weekly_drop = weekly_interact.drop(['Year', 'Direction', 'Direction_num'], axis=1)

# choose a random subset of the predictors

predictor_labels = np.random.choice(weekly_drop.columns,

size=np.random.randint(1, high=weekly_drop.shape[1] + 1),

replace=False)

# choose a random subset of these to transform

trans_predictor_labels = np.random.choice(predictor_labels,

size=np.random.randint(0, len(predictor_labels)),

replace=False)

# choose random transforms

some_transforms = np.random.choice(transforms,

size=len(trans_predictor_labels),

replace=True)

# create the df

df = weekly_interact[predictor_labels].copy()

# transform appropriate columns

for i in range(0, len(trans_predictor_labels)):

# do transformation

df.loc[ : , trans_predictor_labels[i]] = some_transforms[i](df[trans_predictor_labels[i]])

# rename to reflect which transformation was used

df = df.rename({trans_predictor_labels[i]:

some_transforms[i].__name__ + '(' + trans_predictor_labels[i] + ')' }, axis='columns')

return pd.concat([df, weekly_interact['Direction_num']], axis=1)

random_data_tweak(weekly_interact, transforms).head()

| Lag3-Lag5 | power_7(Volume-Today) | power_5(Lag5) | Lag2-Lag5 | power_3(Lag4-Lag5) | sin(Lag4) | Lag2-Today | exp(Lag1-Lag5) | Lag1 | power_5(Lag4-Volume) | exp(Lag1-Today) | Lag4-Today | sin(Lag5-Volume) | Lag3-Today | power_3(Lag3-Lag4) | exp(Lag2) | Direction_num | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 13.713024 | 0.000003 | -42.289684 | -5.476848 | 0.507856 | -0.227004 | -0.424440 | 0.058254 | 0.816 | -0.000045 | 0.802262 | 0.061830 | -0.514081 | 1.062720 | 0.732271 | 4.816271 | 0 |

| 2 | -0.359988 | 0.021456 | -0.012009 | -0.186864 | 0.732271 | 0.713448 | -2.102016 | 1.063781 | -0.270 | -0.199983 | 2.004751 | 10.139136 | -0.034017 | -4.049472 | -236.877000 | 2.261436 | 0 |

| 3 | -3.211776 | 0.099523 | -60.976890 | 1.062720 | -236.877000 | 0.999999 | -0.948780 | 25314.585232 | -2.576 | 0.015863 | 0.000117 | 5.524008 | -0.588434 | 2.867424 | 2.110708 | 0.763379 | 1 |

| 4 | -0.424440 | 0.000175 | 3.884701 | -4.049472 | 2.110708 | 0.728411 | -1.834112 | 250.637582 | 3.514 | 0.002294 | 12.206493 | 0.580992 | 0.251357 | -0.192240 | -0.010695 | 0.076078 | 1 |

| 5 | -2.102016 | 0.001075 | 0.543338 | 2.867424 | -0.010695 | -0.266731 | 4.139492 | 1.787811 | 0.712 | -0.000072 | 2.313441 | -0.318060 | 0.125113 | -3.034528 | 0.336456 | 33.582329 | 1 |

Comparison of Logit, LDA, QDA, and KNN models on a single random data tweak

import sklearn.model_selection as skl_model_selection

def model_comparison():

# tweak data

tweak_df = random_data_tweak(weekly_interact, transforms)

# train test split

X, y = sm.add_constant(tweak_df.drop(['Direction_num'], axis=1).values), tweak_df['Direction_num'].values

X_train, X_test, y_train, y_test = skl_model_selection.train_test_split(X, y)

# dict for models

models = {}

# train param models

models['Logit'] = skl_linear_model.LogisticRegression(solver='lbfgs').fit(X_train, y_train)

models['LDA'] = skl_discriminant_analysis.LinearDiscriminantAnalysis().fit(X_train, y_train)

models['QDA'] = skl_discriminant_analysis.QuadraticDiscriminantAnalysis().fit(X_train, y_train)

# train KNN models for K = 1,..,5

for i in range(1, 6):

models['KNN' + stri.] = skl_neighbors.KNeighborsClassifier(n_neighbors=i).fit(X_train, y_train)

return {'predictors': tweak_df.columns, 'comparison': confusion_comparison(X_test, y_test, models)}

model_comparison()

Comparison of Logit, LDA, QDA, and KNN models over data tweaks

def model_comparisons(n):

# running list of predictors and dfs from each comparison

predictors_list = []

dfs = []

# iterate comparisons

for i in range(n):

# get comparison result

result = model_comparison()

predictors_list += [result['predictors']]

# set MultiIndex

df = result['comparison']

df['Instance'] = i

df = df.reset_index()

df = df.set_index(['Instance', 'Model'])

# add results to running lists

dfs += [df]

return {'predictors': predictors_list, 'comparisons': pd.concat(dfs)}

results = model_comparisons(1000)

Here are the first 3 comparisons:

comparisons_df = results['comparisons']

comparisons_df.head(21)

| accuracy | error rate | null error | TP rate | FP rate | TN rate | FN rate | precision | prevalence | ||

|---|---|---|---|---|---|---|---|---|---|---|

| Instance | Model | |||||||||

| 0 | Logit | 0.560440 | 0.439560 | 0.549451 | 0.666667 | 0.466667 | 0.430894 | 0.406504 | 0.588235 | 0.549451 |

| LDA | 0.948718 | 0.051282 | 0.549451 | 1.000000 | 0.093333 | 0.886179 | 0.000000 | 0.914634 | 0.549451 | |

| QDA | 0.450549 | 0.549451 | 0.549451 | 0.000000 | 0.000000 | 1.000000 | 1.219512 | NaN | 0.549451 | |

| KNN1 | 0.714286 | 0.285714 | 0.549451 | 0.760000 | 0.280000 | 0.658537 | 0.292683 | 0.730769 | 0.549451 | |

| KNN2 | 0.688645 | 0.311355 | 0.549451 | 0.553333 | 0.120000 | 0.853659 | 0.544715 | 0.821782 | 0.549451 | |

| KNN3 | 0.703297 | 0.296703 | 0.549451 | 0.740000 | 0.280000 | 0.658537 | 0.317073 | 0.725490 | 0.549451 | |

| KNN4 | 0.699634 | 0.300366 | 0.549451 | 0.653333 | 0.200000 | 0.756098 | 0.422764 | 0.765625 | 0.549451 | |

| KNN5 | 0.703297 | 0.296703 | 0.549451 | 0.760000 | 0.300000 | 0.634146 | 0.292683 | 0.716981 | 0.549451 | |

| 1 | Logit | 0.937729 | 0.062271 | 0.523810 | 0.979021 | 0.097902 | 0.892308 | 0.023077 | 0.909091 | 0.523810 |

| LDA | 0.695971 | 0.304029 | 0.523810 | 0.965035 | 0.545455 | 0.400000 | 0.038462 | 0.638889 | 0.523810 | |

| QDA | 0.476190 | 0.523810 | 0.523810 | 0.000000 | 0.000000 | 1.000000 | 1.100000 | NaN | 0.523810 | |

| KNN1 | 0.706960 | 0.293040 | 0.523810 | 0.769231 | 0.328671 | 0.638462 | 0.253846 | 0.700637 | 0.523810 | |

| KNN2 | 0.710623 | 0.289377 | 0.523810 | 0.587413 | 0.139860 | 0.846154 | 0.453846 | 0.807692 | 0.523810 | |

| KNN3 | 0.706960 | 0.293040 | 0.523810 | 0.790210 | 0.349650 | 0.615385 | 0.230769 | 0.693252 | 0.523810 | |

| KNN4 | 0.695971 | 0.304029 | 0.523810 | 0.650350 | 0.230769 | 0.746154 | 0.384615 | 0.738095 | 0.523810 | |

| KNN5 | 0.725275 | 0.274725 | 0.523810 | 0.825175 | 0.349650 | 0.615385 | 0.192308 | 0.702381 | 0.523810 | |

| 2 | Logit | 0.454212 | 0.545788 | 0.545788 | 0.000000 | 0.000000 | 1.000000 | 1.201613 | NaN | 0.545788 |

| LDA | 0.967033 | 0.032967 | 0.545788 | 0.959732 | 0.020134 | 0.975806 | 0.048387 | 0.979452 | 0.545788 | |

| QDA | 0.454212 | 0.545788 | 0.545788 | 0.000000 | 0.000000 | 1.000000 | 1.201613 | NaN | 0.545788 | |

| KNN1 | 0.501832 | 0.498168 | 0.545788 | 0.510067 | 0.422819 | 0.491935 | 0.588710 | 0.546763 | 0.545788 | |

| KNN2 | 0.487179 | 0.512821 | 0.545788 | 0.308725 | 0.248322 | 0.701613 | 0.830645 | 0.554217 | 0.545788 |

Here are the predictors used for the first 3 comparisons:

predictors_list = results['predictors']

predictors_list[0:3]

[Index(['Lag2-Today', 'Lag4-Volume', 'Lag2-Lag3', 'Volume-Today', 'Lag2',

'power_7(Lag1-Volume)', 'Lag1-Lag2', 'Lag2-Volume', 'Lag4-Today',

'sin(Lag3-Today)', 'Lag3-Lag4', 'Lag5-Volume', 'Today',

'power_5(Lag3-Lag5)', 'Lag1-Lag5', 'Lag4', 'Direction_num'],

dtype='object'),

Index(['Lag3-Lag5', 'Lag5-Today', 'Lag1', 'sin(Lag2-Volume)', 'Lag2-Today',

'power_5(Volume)', 'Lag4-Lag5', 'Lag1-Lag2', 'power_5(Lag2-Lag3)',

'Lag3-Today', 'Lag3-Volume', 'Volume-Today', 'Lag1-Today',

'Direction_num'],

dtype='object'),

Index(['power_3(Lag2-Lag3)', 'Lag1-Today', 'Lag4-Volume', 'sin(Lag1-Lag2)',

'power_7(Lag2-Today)', 'Lag1', 'exp(Lag2-Lag4)', 'power_3(Volume)',

'exp(Lag3-Lag5)', 'exp(Lag5)', 'power_5(Lag1-Lag5)', 'Today',

'Lag1-Lag3', 'Lag4-Today', 'power_5(Lag5-Today)', 'exp(Lag3-Lag4)',

'power_7(Lag3-Today)', 'sin(Lag2)', 'sin(Volume-Today)',

'power_3(Lag2-Volume)', 'Lag1-Lag4', 'power_7(Lag4-Lag5)',

'exp(Lag5-Volume)', 'Direction_num'],

dtype='object')]

Analysis of Comparisons

Analyzing accuracy across models

Summary statistics

grouped_by_model = comparisons_df.groupby(level=1)

grouped_by_model.mean()

| accuracy | error rate | null error | TP rate | FP rate | TN rate | FN rate | precision | prevalence | |

|---|---|---|---|---|---|---|---|---|---|

| Model | |||||||||

| KNN1 | 0.626147 | 0.373853 | 0.556381 | 0.668314 | 0.342757 | 0.574424 | 0.418527 | 0.662625 | 0.55615 |

| KNN2 | 0.601912 | 0.398088 | 0.556381 | 0.463810 | 0.180901 | 0.775631 | 0.676137 | 0.707457 | 0.55615 |

| KNN3 | 0.629945 | 0.370055 | 0.556381 | 0.690867 | 0.358510 | 0.555069 | 0.390503 | 0.661137 | 0.55615 |

| KNN4 | 0.615769 | 0.384231 | 0.556381 | 0.544830 | 0.237261 | 0.705825 | 0.574505 | 0.691635 | 0.55615 |

| KNN5 | 0.631011 | 0.368989 | 0.556381 | 0.706117 | 0.371881 | 0.538619 | 0.371593 | 0.658446 | 0.55615 |

| LDA | 0.726355 | 0.273645 | 0.556381 | 0.942929 | 0.437290 | 0.456703 | 0.073307 | 0.717898 | 0.55615 |

| Logit | 0.551216 | 0.448784 | 0.556381 | 0.368049 | 0.176416 | 0.782584 | 0.797881 | 0.697051 | 0.55615 |

| QDA | 0.462040 | 0.537960 | 0.556381 | 0.085262 | 0.053065 | 0.933012 | 1.151742 | 0.619088 | 0.55615 |

grouped_by_model.mean().accuracy.sort_values(ascending=False)

Model

LDA 0.726355

KNN5 0.631011

KNN3 0.629945

KNN1 0.626147

KNN4 0.615769

KNN2 0.601912

Logit 0.551216

QDA 0.462040

Name: accuracy, dtype: float64

Let’s look at summary statistics for accuracy

grouped_by_model.accuracy.describe()

| count | mean | std | min | 25% | 50% | 75% | max | |

|---|---|---|---|---|---|---|---|---|

| Model | ||||||||

| KNN1 | 1000.0 | 0.626147 | 0.111154 | 0.435897 | 0.545788 | 0.600733 | 0.684982 | 1.000000 |

| KNN2 | 1000.0 | 0.601912 | 0.112694 | 0.421245 | 0.516484 | 0.578755 | 0.659341 | 1.000000 |

| KNN3 | 1000.0 | 0.629945 | 0.110973 | 0.443223 | 0.549451 | 0.604396 | 0.682234 | 1.000000 |

| KNN4 | 1000.0 | 0.615769 | 0.113840 | 0.410256 | 0.531136 | 0.589744 | 0.670330 | 0.996337 |

| KNN5 | 1000.0 | 0.631011 | 0.112222 | 0.439560 | 0.549451 | 0.600733 | 0.692308 | 1.000000 |

| LDA | 1000.0 | 0.726355 | 0.177813 | 0.476190 | 0.556777 | 0.699634 | 0.941392 | 0.996337 |

| Logit | 1000.0 | 0.551216 | 0.186576 | 0.369963 | 0.439560 | 0.468864 | 0.553114 | 1.000000 |

| QDA | 1000.0 | 0.462040 | 0.072413 | 0.369963 | 0.428571 | 0.446886 | 0.468864 | 0.967033 |

Interesting – all models were able to get very close to or achieve 100% accuracy at least once.

TO DO: Try to find similarities in predictors/transformations for the instances which gave maximum classification accuracy

Let’s look at some distributions.

Distributions of accuracy across models

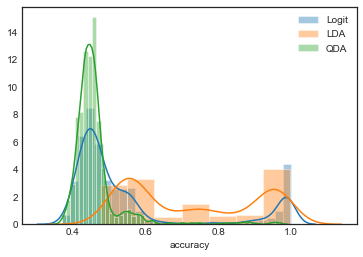

Parametric models

import seaborn as sns

sns.set_style('white')

param_models = ['Logit', 'LDA', 'QDA']

for model_name in param_models:

sns.distplot(grouped_by_model.accuracy.get_group(model_name), label=model_name)

plt.legend()

<matplotlib.legend.Legend at 0x1a254db860>

Observations

- There are some interesting peaks here – the distributions look bimodal.

- Both Logit and QDA models are highly concentrated in low accuracy, but LDA is more spread out

TO DO: Try to find similarities in predictors/transformations for the instances clustered around these two modes

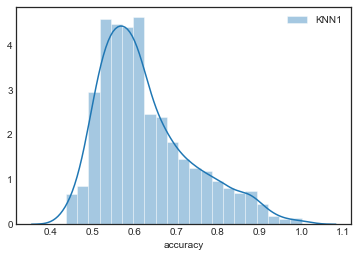

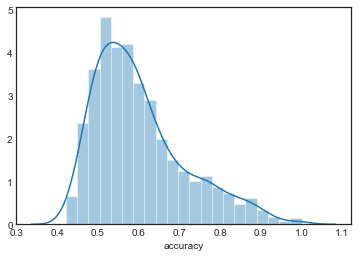

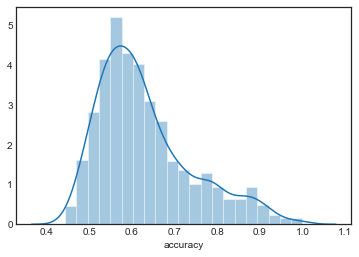

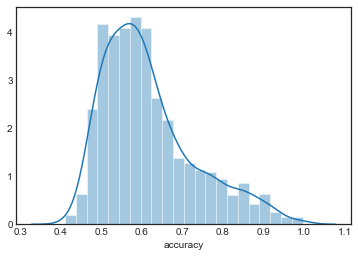

KNN models

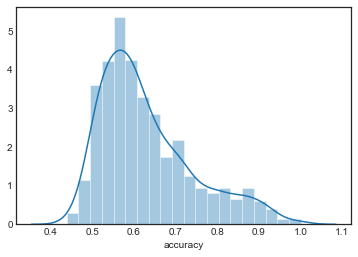

sns.distplot(grouped_by_model.accuracy.get_group('KNN1'), label='KNN1')

plt.legend()

<matplotlib.legend.Legend at 0x1a252924a8>

sns.distplot(grouped_by_model.accuracy.get_group('KNN2'), label='KNN2')

<matplotlib.axes._subplots.AxesSubplot at 0x1a2a6e6940>

sns.distplot(grouped_by_model.accuracy.get_group('KNN3'), label='KNN3')

<matplotlib.axes._subplots.AxesSubplot at 0x1a25ce2cc0>

sns.distplot(grouped_by_model.accuracy.get_group('KNN4'), label='KNN4')

<matplotlib.axes._subplots.AxesSubplot at 0x1a2569ad30>

sns.distplot(grouped_by_model.accuracy.get_group('KNN5'), label='KNN5')

<matplotlib.axes._subplots.AxesSubplot at 0x1a25ca3dd8>

The distributions are all very similar, although they appear to become more concentrated as increases.